Real Estate Investor Insights

When investors start comparing mortgage options, the first thing most of them look at is the rate. Conventional loan at 7.25%. DSCR loan at 7.875%. The conventional loan wins, right? Not necessarily. And for investors who are serious about building a portfolio, not usually. The rate is one number. T

Financing Higher-Density Rental Strategies for Scalable Portfolio Growth Real estate investment dynamics across Idaho are evolving as population migration, affordability pressures, and rising acquisition costs reshape traditional rental performance metrics. Investors who previously relied on long-te

If you are a real estate investor looking to build a rental portfolio in Idaho, one financing tool is separating the investors who are scaling from the ones who are stuck: the DSCR loan. No tax returns. No W2s. No debt-to-income calculations. Just the property’s cash flow qualifying the deal. Idaho’

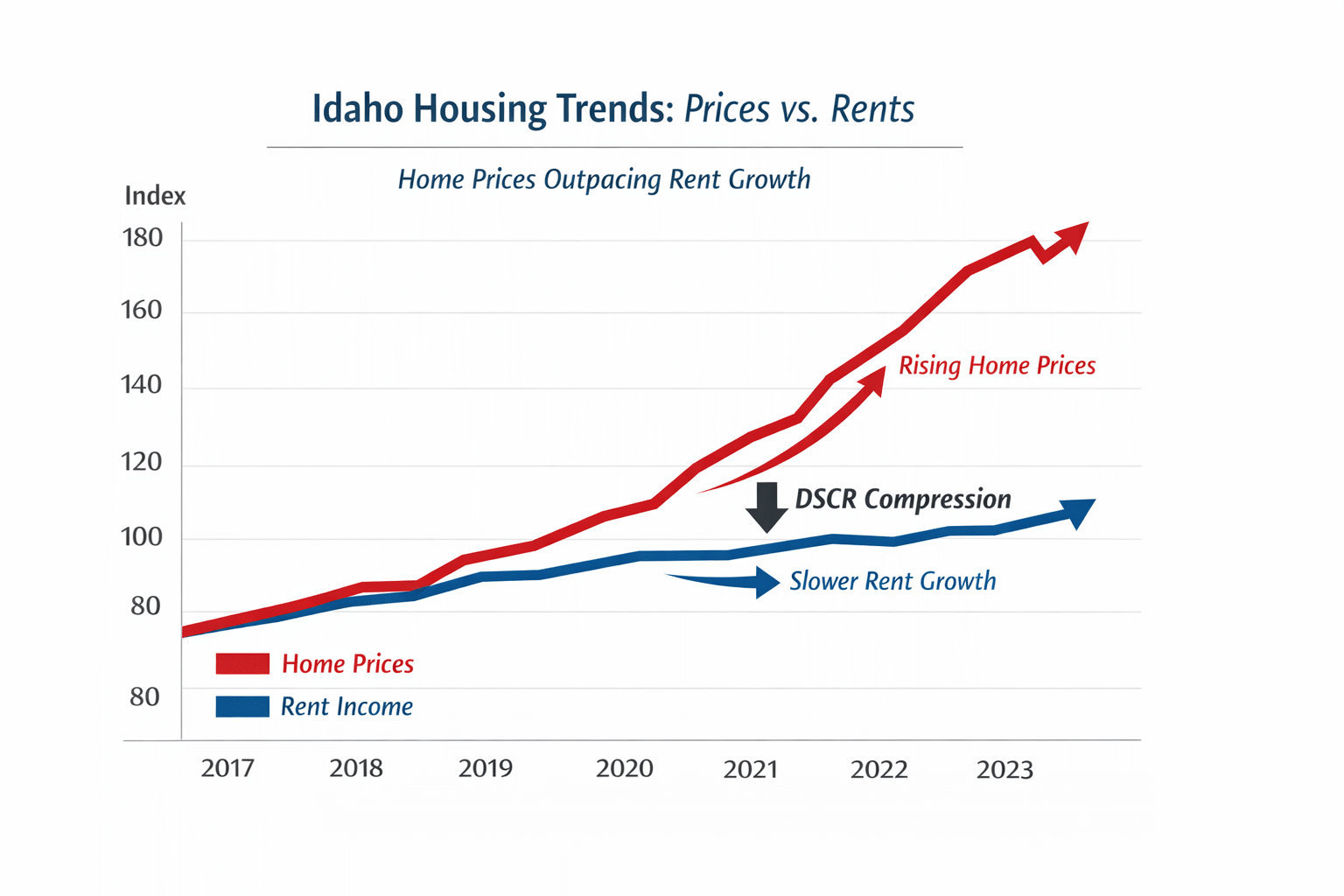

Idaho investors are not struggling because opportunities disappeared.They are struggling because financing assumptions have not kept pace with how the market now behaves. Property values in many areas — especially across the Treasure Valley — have risen faster than achievable rental income. In contr

A Vacant Property. Zero Rental History. A 1.53 DSCR Ratio the Day Rehab Was Complete. Most investors assume a vacant property cannot qualify for a DSCR cash-out refinance. No tenants. No rental income history. No executed leases. In conventional financing that assumption is correct — and it is the r

Idaho’s most productive DSCR markets are not where most investors are looking. While attention concentrates on Boise and Meridian rural Idaho is quietly delivering some of the strongest debt service coverage ratios in the Mountain West. Twin Falls, Pocatello, Idaho Falls, Lewiston, Sandpoint, and Ca

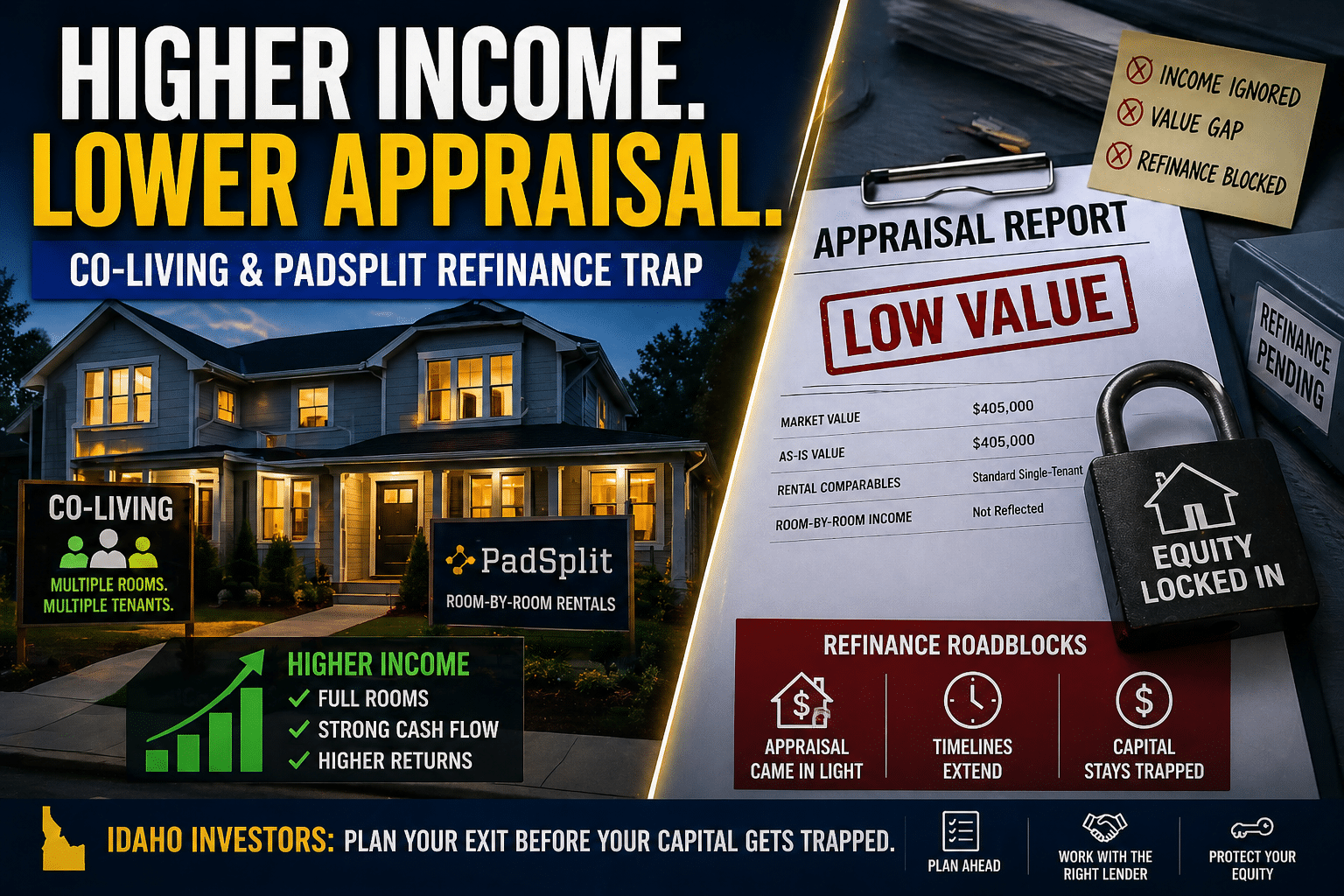

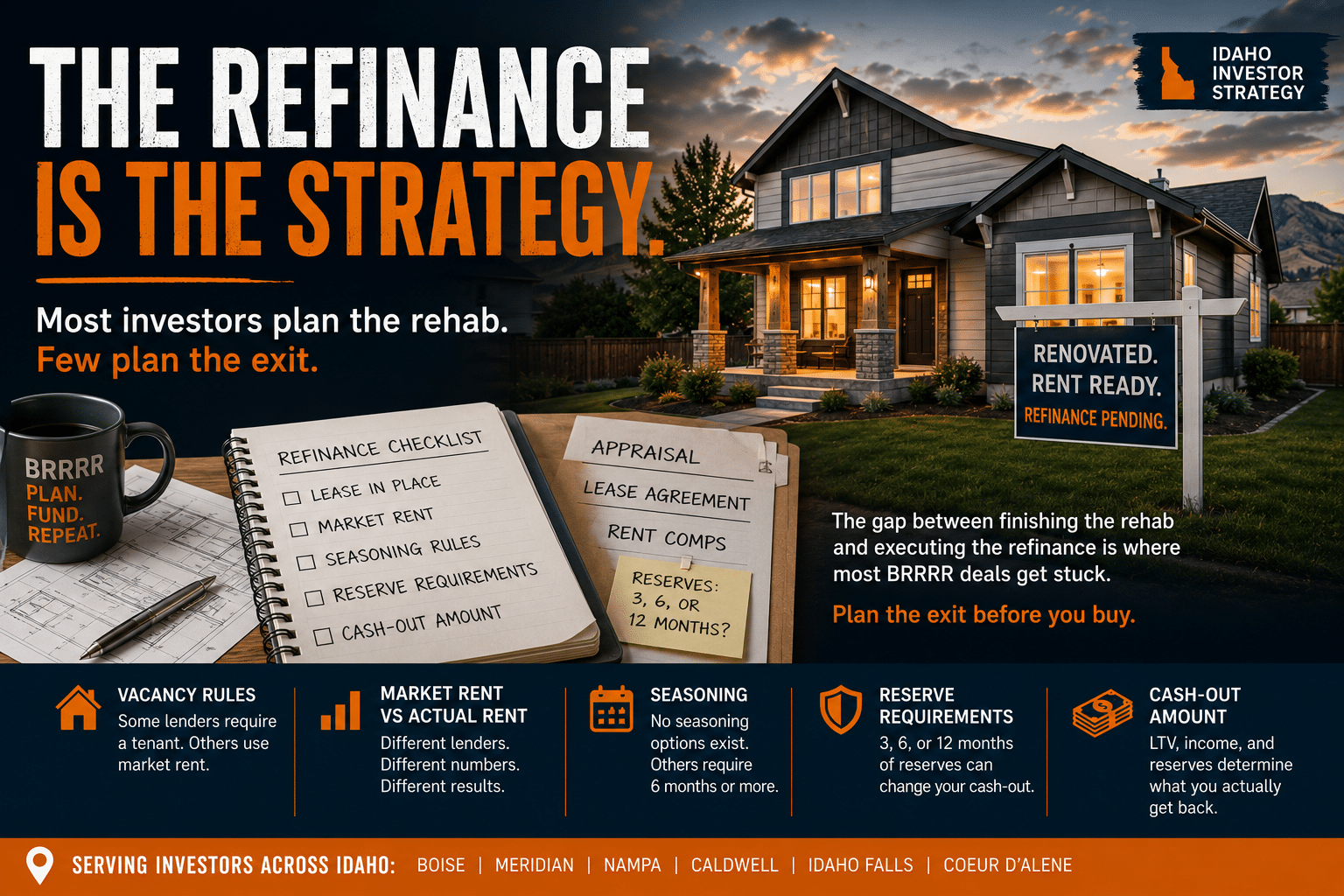

The investors who run into the most trouble with co-living and PadSplit deals in Idaho are not the ones who made mistakes on the purchase. They are the ones who executed the acquisition correctly, improved the property, filled the rooms, and then found out the refinance did not work the way they exp

Most investors think DSCR loans are simple.Property income covers the payment.Loan gets approved. That’s not where deals fall apart. They fall apart in the parts no one explains. Because DSCR loans don’t work one way.They work differently depending on how the deal is structured. And that’s what most

I heard it again last night at an investor meeting. “I’m concerned about my liquidity. If I buy this property in cash, how quickly can I get my money back out after closing?” It’s a valid concern, and it comes up often. Most of the time it’s coming from someone who has spent all of […]

Most investors searching for DSCR lenders in Idaho assume the loan works the same regardless of where they go. The qualification is based on the property income and the DSCR ratio. That part is consistent. What is not consistent is how each lender interprets those inputs and what they will actually

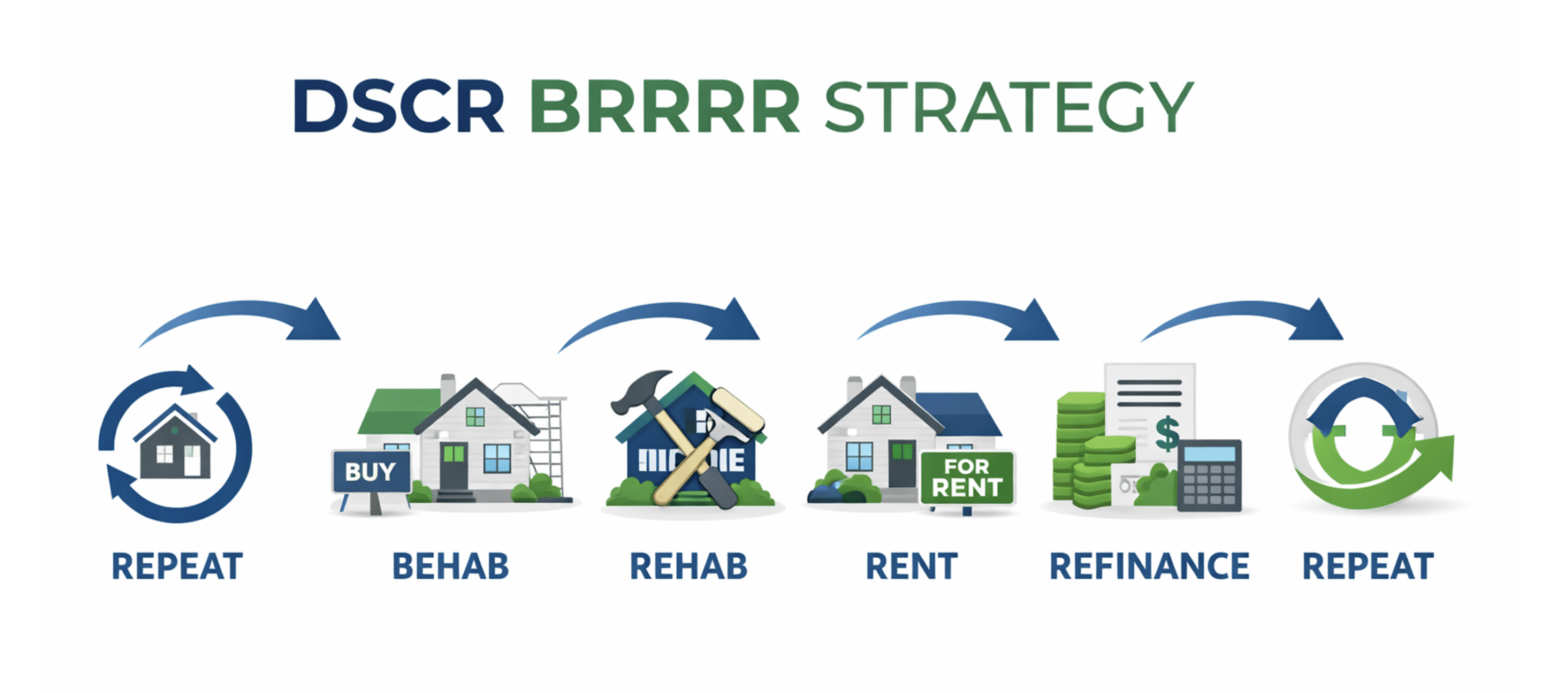

Most investors who come to me with BRRRR deals are not failing on the buy. They are failing on the refinance, and they usually do not realize it until their capital is already stuck in the deal. The DSCR BRRRR strategy in Idaho changes that equation, but only if the refinance is structured before th

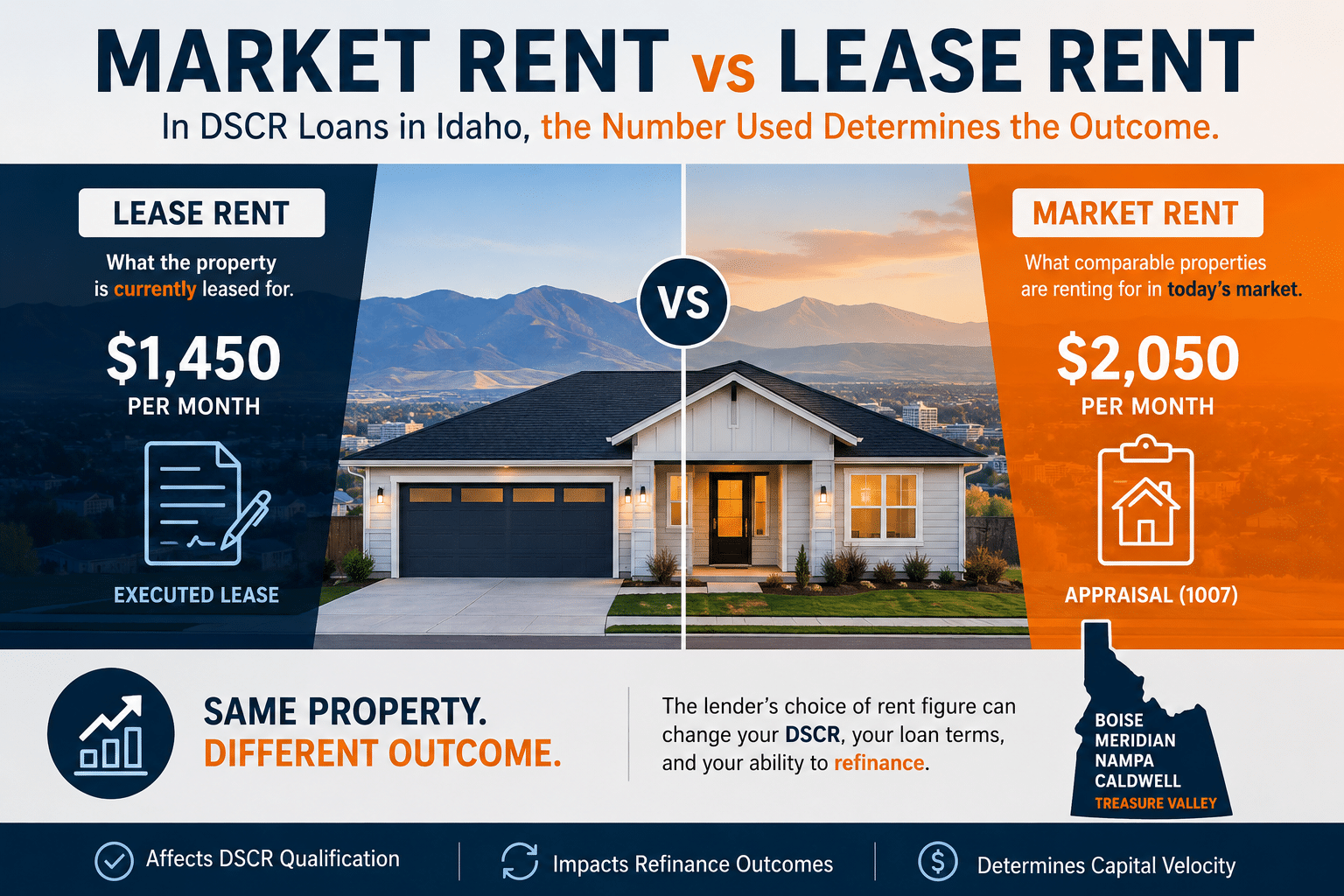

On almost every DSCR loan, two rent numbers exist at the same time, one from the lease and one from the appraisal. The outcome of the deal depends on which one the lender chooses to use. Most investors do not think about this until the refinance is already in motion. By that point, the deal [&hellip

Most people hear two words and stop there. No income. That becomes the whole story. No tax returns. No W2s. No debt-to-income wall. Sounds simple. It is not that simple. A DSCR loan is not valuable because it removes paperwork. It is valuable because it changes how an investment property is judged a

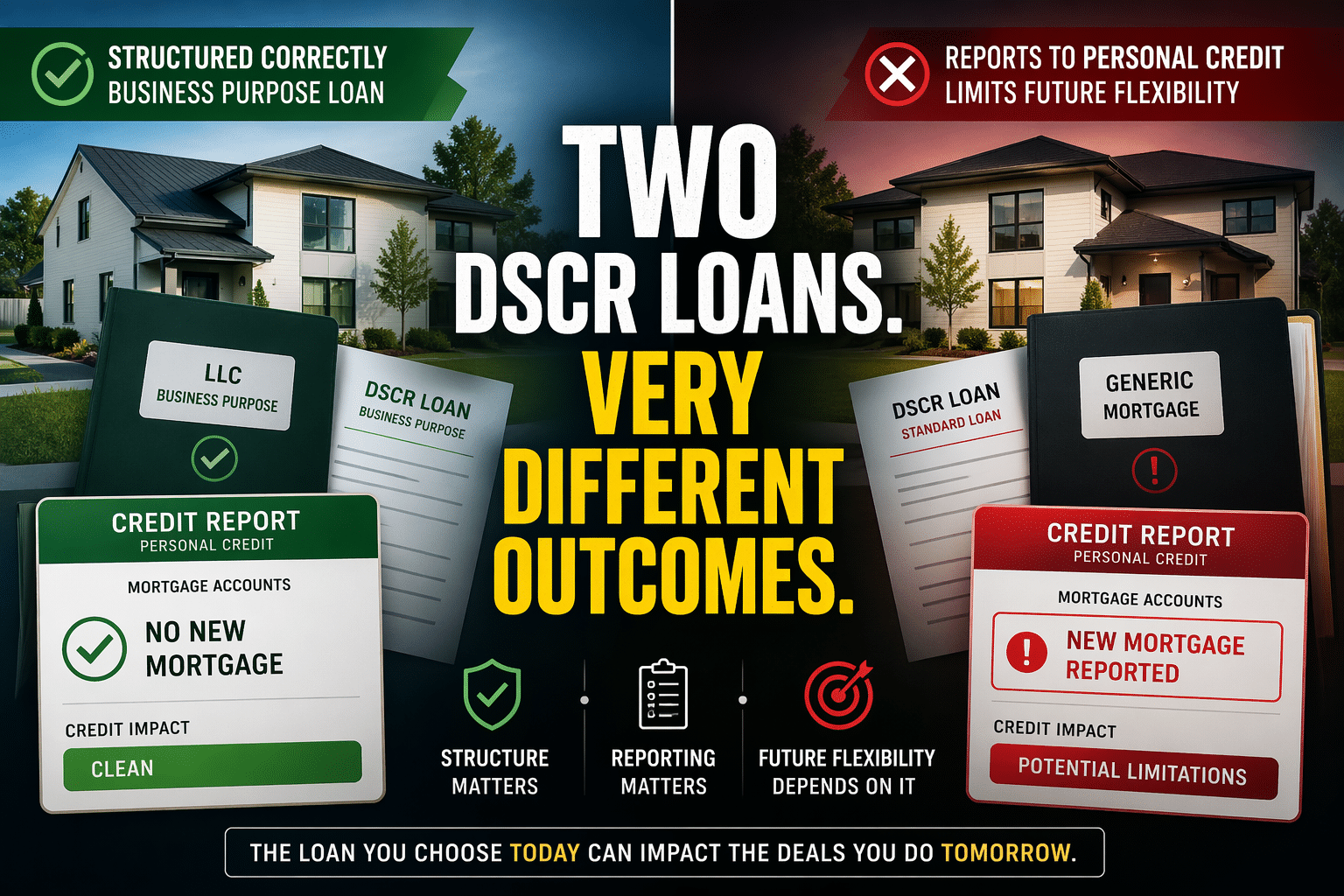

Most investors think if they close a DSCR loan in an LLC, it automatically stays off their personal credit. That assumption costs people later. Because not all DSCR lenders handle these loans the same way. Some structure investor loans through true business-purpose lending platforms. Others run DSCR

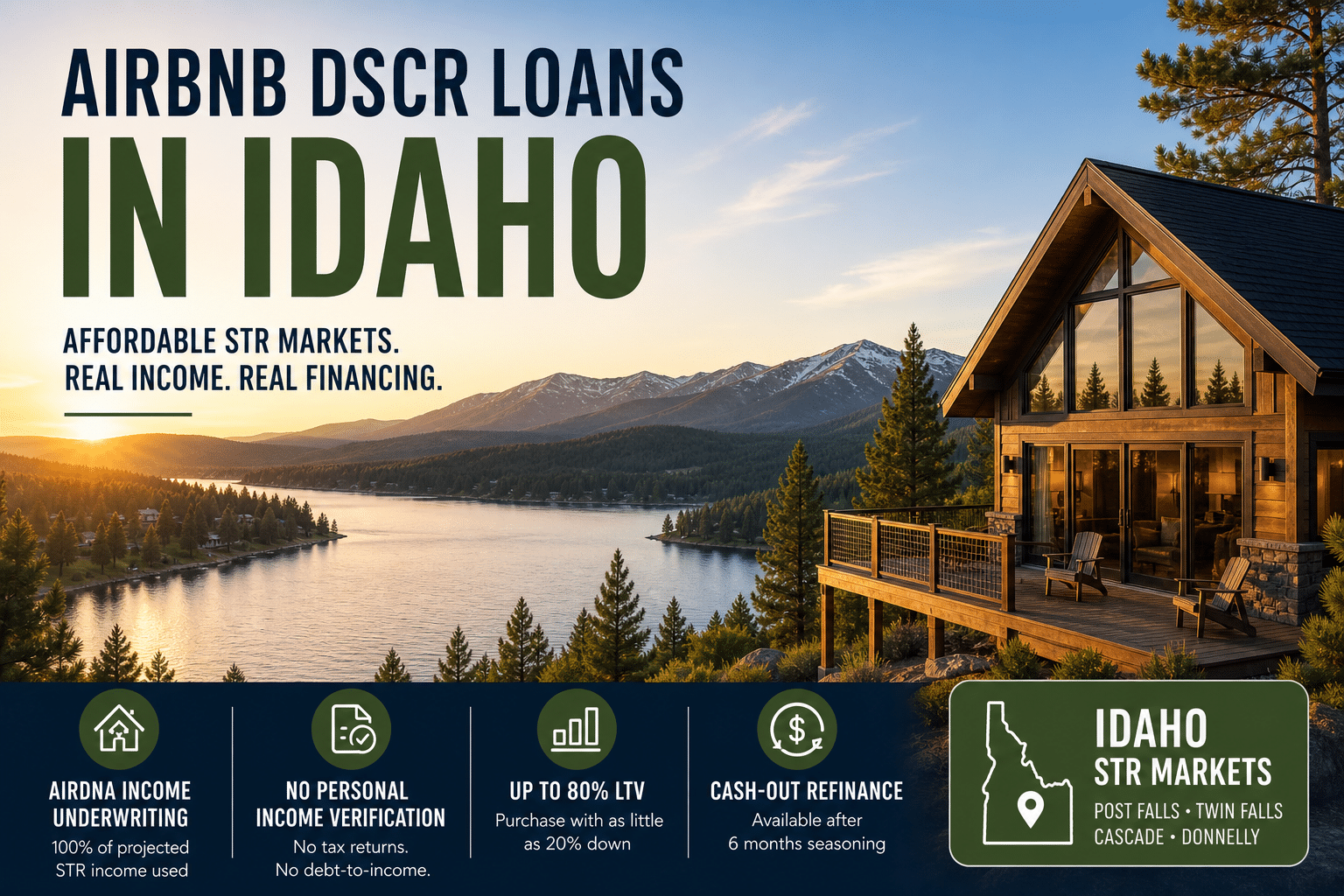

Idaho’s short-term rental market isn’t just Coeur d’Alene and Sun Valley. Those markets get the attention. But the investors finding the strongest returns right now are looking at something different. Markets where entry prices don’t require a seven-figure down payment. Markets where tourism demand

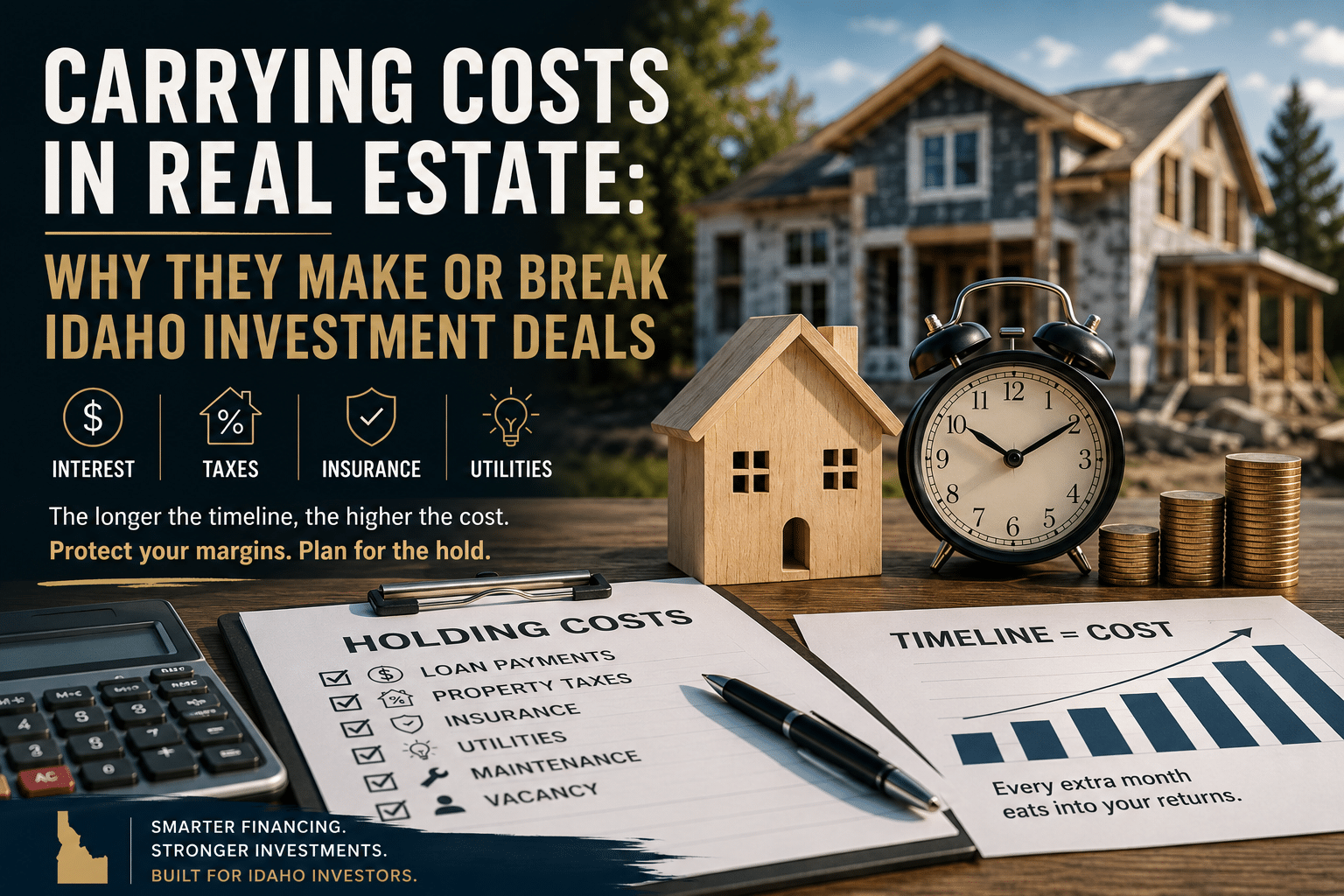

Most Idaho investors who get into trouble on a deal did not make a mistake on the purchase. They bought at a reasonable price, estimated the rehab correctly, and had a realistic rent target. The deal made sense when they underwrote it. Most investment deals do not fail at acquisition. They fail in t

On almost every DSCR loan, two different rent figures exist at the same time. One comes from the lease. The other comes from the appraisal. The outcome of the deal depends on which one the lender chooses to use. Most investors do not think about this distinction until the refinance is already in mot

Most investors who get surprised by reserve requirements did not miss anything obvious. They checked the purchase price, confirmed the rent, verified the credit score, and ran the DSCR ratio. The deal qualified. Then the file hit underwriting and the conversation shifted to a number they had not ful

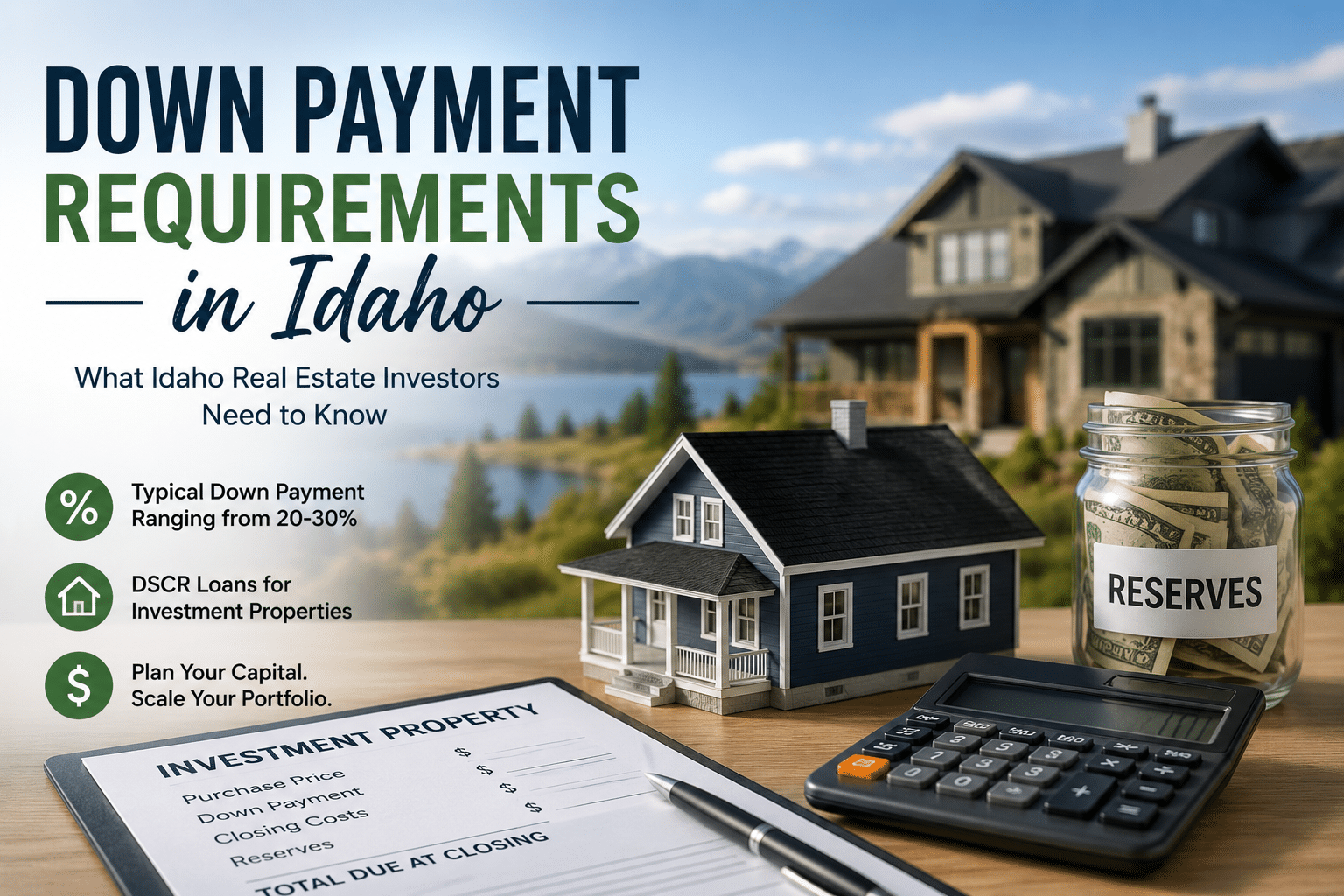

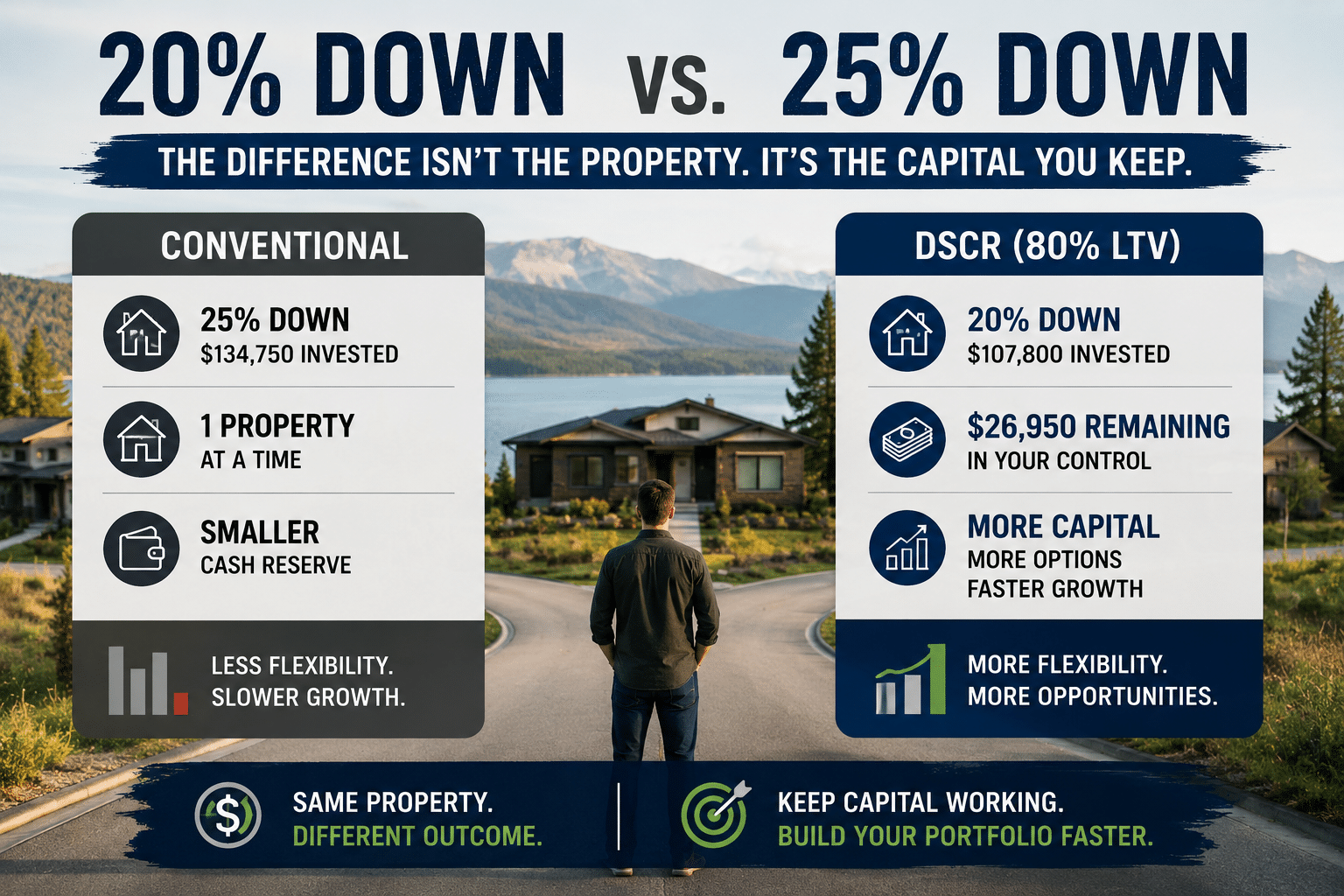

Understand what 80% LTV means for your down payment, capital availability, and long-term portfolio growth. Most investors think about the down payment as the price of entry. It isn’t. It’s a capital allocation decision. And on DSCR loans in Idaho, that decision has a specific number attached to it t

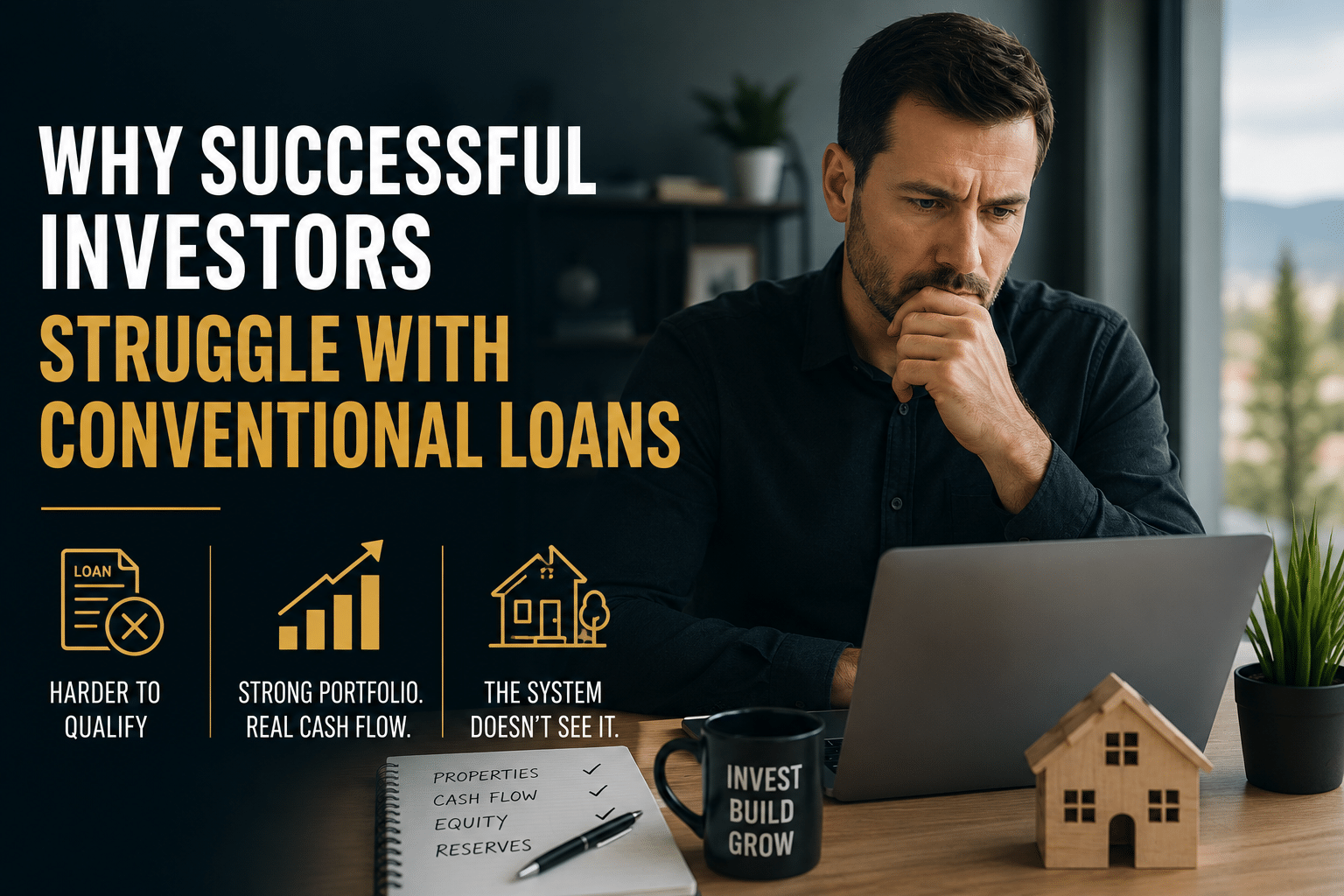

Most investors assume qualifying for financing gets easier as the portfolio grows. The properties are performing, cash flow is improving, net worth is increasing, and reserves are healthy. Then the investor applies for another conventional loan and discovers the paperwork looks worse than it did whe

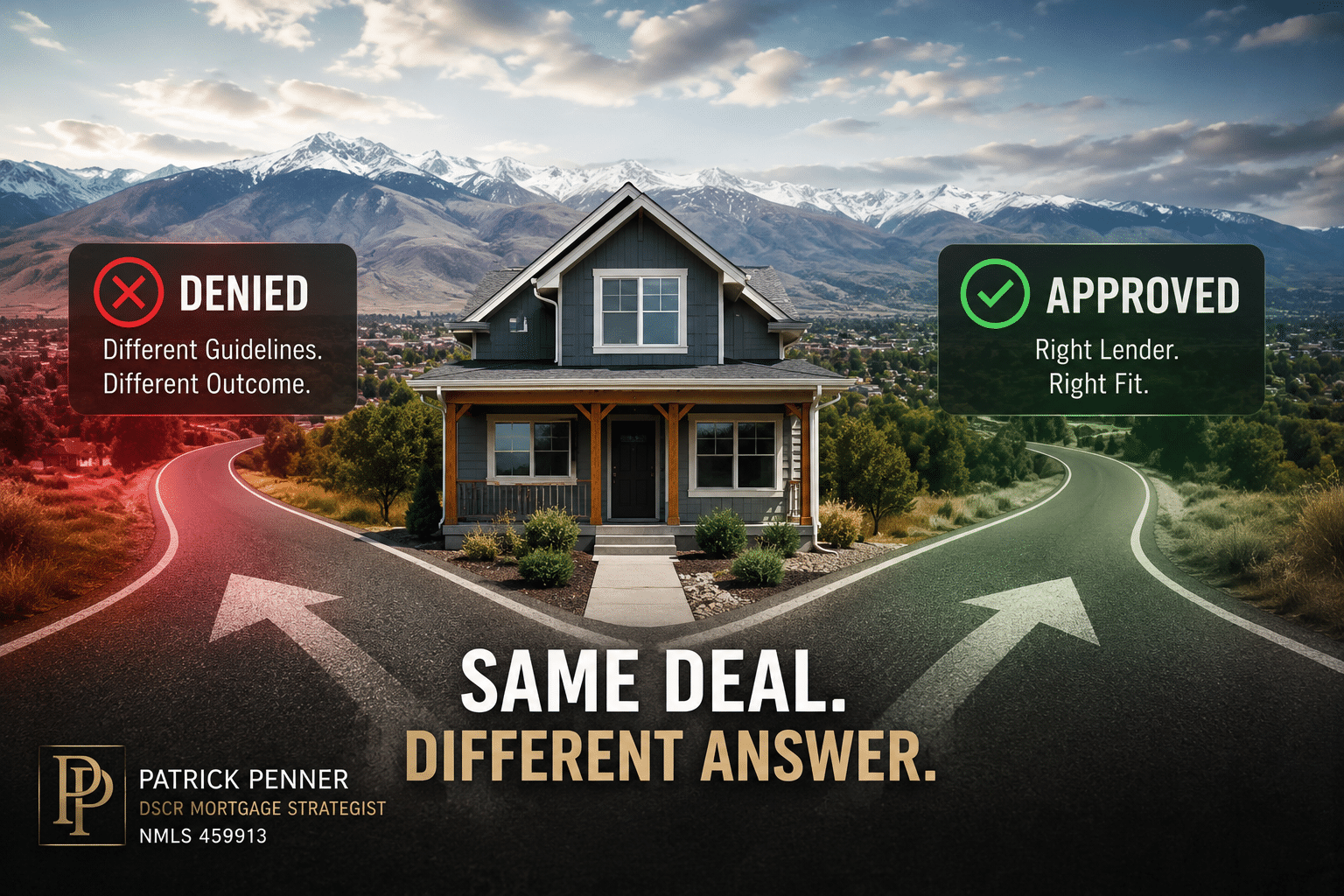

Most Idaho real estate investors have lived some version of this story. You find a deal, you run the numbers, you submit it, and you hear that the property does not qualify. A few weeks later you take the same property to a different lender and it closes. Same house. Same rent. Same borrower. Two [&

Most investors think the hard part of a BRRRR deal is the rehab. Finding the property, managing contractors, staying on budget, and getting the work done on schedule absorb almost all of the attention. Once the project wraps, the assumption is that the easy part begins. The refinance pulls the capit

Most Idaho real estate investors begin a DSCR loan conversation the same way. “What’s your rate?” It’s a fair question. After all, interest rates matter, and no investor wants to pay more than necessary to finance a property. Many investors also assume they’re comparing the same loan when they reque

Most people shopping for financing are asking the wrong question. They want to know the rate. They want to know if they qualify. They’re thinking like borrowers. For most of their lives, borrowing is all they’ve done: a mortgage on a primary residence, a car loan, maybe a student loan. Those loans a