DSCR Loan Down Payment Requirements in Idaho

Understand what 80% LTV means for your down payment, capital availability, and long-term portfolio growth.

Most investors think about the down payment as the price of entry.

It isn’t.

It’s a capital allocation decision. And on DSCR loans in Idaho, that decision has a specific number attached to it that most investors aren’t fully accounting for before they go under contract.

Here’s what 80% LTV actually means in practice across Idaho investment property markets.

For a full breakdown of how DSCR loans work in Idaho:

https://www.dscrfinancing.com/dscr-loans-idaho/

The Conventional Default and Why It Costs You

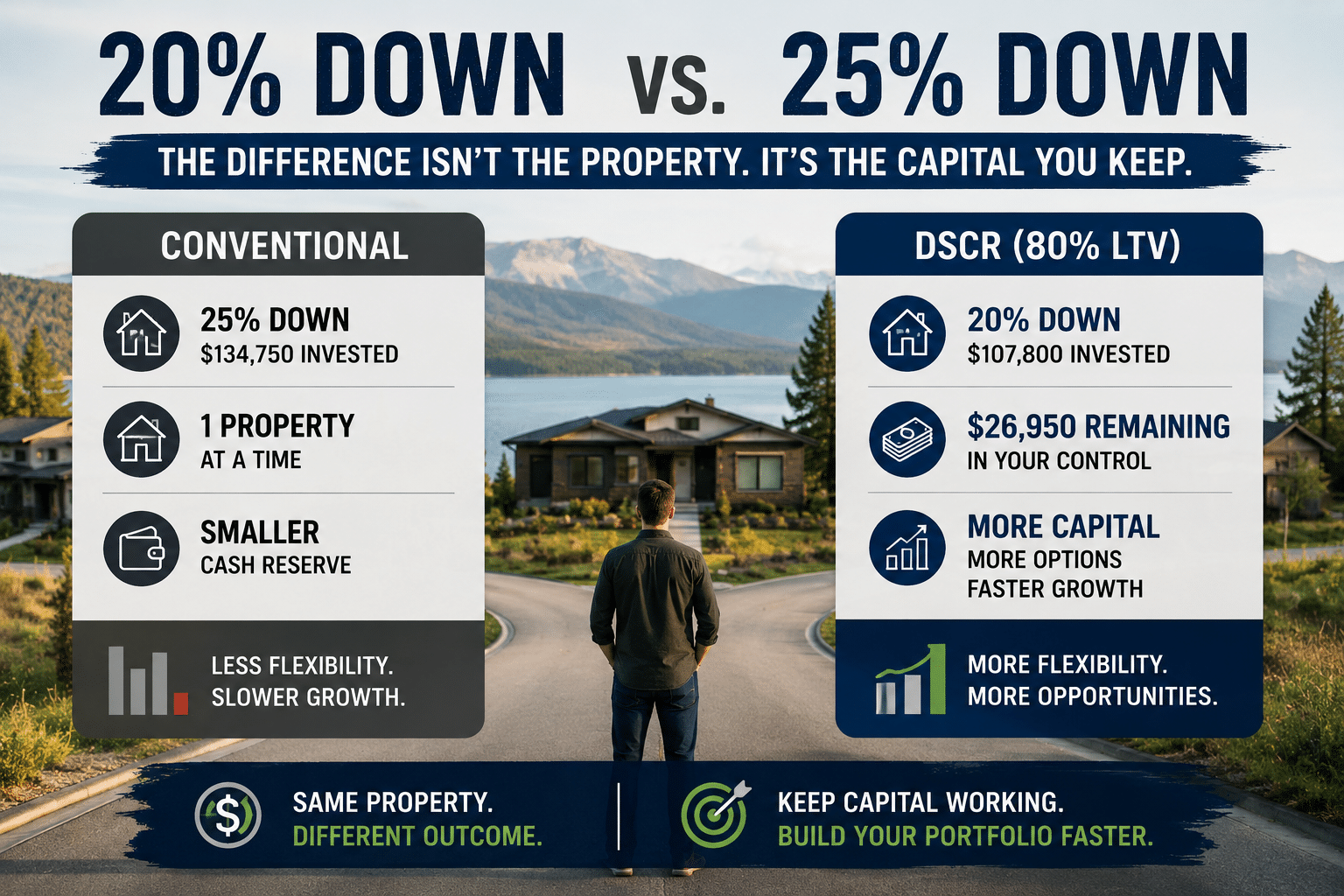

Conventional investment property financing often requires 20% to 25% down depending on property type, with two-to-four-unit properties commonly requiring 25%.

Most investors accept that standard without questioning whether a better structure exists.

On a $539,000 property in Post Falls, 25% down is $134,750.

That capital is now tied up in one property. It’s not available for the next deal. It’s not sitting in reserves. It’s not deployed anywhere else in your portfolio.

That’s the real cost of conventional financing. Not the rate. The capital.

What 80% LTV Changes

Many DSCR programs in Idaho currently allow up to 80% LTV on qualifying single-family investment properties with a 700 minimum credit score.

That moves the down payment from 25% to 20%.

Five percent sounds small. In Idaho markets, it isn’t.

Post Falls

25% down: $134,750

20% down: $107,800

Capital freed: $26,950

Coeur d’Alene

25% down: $150,000

20% down: $120,000

Capital freed: $30,000

Cascade

25% down: $130,000

20% down: $104,000

Capital freed: $26,000

Donnelly

25% down: $170,000

20% down: $136,000

Capital freed: $34,000

Boise

25% down: $122,500

20% down: $98,000

Capital freed: $24,500

That freed capital doesn’t disappear. It stays in your control. And what you do with it determines how fast your portfolio grows.

What Investors Do With the Difference

The investors scaling fastest in Idaho aren’t finding better deals.

They’re financing smarter.

Two investors. Same $135,000 in available capital. Different financing structures.

Investor A uses conventional financing at 25% down and deploys nearly all available capital into one acquisition. At that point, reserves are tighter and the timeline for the next purchase often depends on additional savings or waiting for equity growth.

Investor B uses DSCR financing at 80% LTV on the same property and retains roughly $27,000 in available capital. That remaining capital can strengthen reserves, support a second acquisition, or provide flexibility for the next opportunity.

Understanding reserve requirements becomes increasingly important as leverage and portfolio size grow.

Learn more about DSCR reserve requirements in Idaho:

https://www.dscrfinancing.com/dscr-reserve-requirements-idaho/

Same market. Same capital. Different outcome.

A Note on Leverage

Higher leverage is not automatically better.

More leverage can mean stronger portfolio growth, but it can also mean higher payments and different pricing. The question is not whether more leverage is good or bad. The question is whether keeping capital available creates more value than committing it to a larger down payment.

For investors focused on scaling, the answer is usually yes. For investors prioritizing cash flow on a single property, a larger down payment may make more sense. The right structure depends on the plan.

Why DSCR Produces This Structure

Conventional lenders tie leverage to the borrower.

Your income. Your debt load. Your tax returns. Your DTI.

DSCR lenders tie leverage to the property.

Does the rental income support the debt? That’s the question. If yes, the loan moves forward regardless of how many properties you already own, how your income is structured, or whether you took heavy depreciation last year.

That’s why self-employed investors, portfolio builders, and investors with large depreciation positions consistently choose DSCR over conventional. The property qualifies on its own performance. Your personal financial picture stays out of it.

No W2s. No tax returns. No debt-to-income calculation.

Credit Score and LTV: Where You Land Matters

Not every borrower accesses 80% LTV.

Here’s how it breaks down:

620 credit score: programs available, lower leverage

660 credit score: 75% LTV available

700 credit score: 80% LTV available through select lenders

720+ credit score: best pricing, strongest lender options

Where you land on that range directly affects how much capital stays in your control on every deal. A borrower at 695 who gets to 700 before closing doesn’t just improve their rate. They free up thousands in down payment capital across every acquisition they make from that point forward.

STR Properties: Same Structure, Different Income Calculation

For short-term rental properties in Idaho, the 80% LTV structure applies with one key difference.

Income is calculated using AirDNA projected revenue instead of a lease comp.

That matters because STR income in markets like Post Falls, Cascade, and Donnelly meaningfully exceeds what a long-term lease would produce. Using AirDNA means the full income picture goes into underwriting. Not a discounted version of it.

The capital difference at 80% LTV applies equally to STR and long-term rental purchases.

More on STR DSCR financing in Idaho’s accessible markets here:

https://www.dscrfinancing.com/airbnb-dscr-loans-idaho/

The Down Payment Decision Is a Portfolio Decision

Most investors make the down payment decision property by property.

The investors building the strongest portfolios make it at the portfolio level.

Every dollar tied up in a down payment above the minimum is a dollar not available for the next acquisition. That math compounds over time. Three properties into a portfolio, the investor who consistently used 80% LTV has materially more capital in play than the investor who defaulted to 25% down every time.

That’s not theoretical. That’s arithmetic.

Frequently Asked Questions

What is the minimum down payment on a DSCR loan in Idaho?

20% on qualifying single family properties with a 700 minimum credit score. That’s 80% LTV. Lower credit profiles have options but at different leverage.

Does the down payment requirement change for STR properties?

The LTV structure is the same. The income calculation changes. STR properties use AirDNA projected revenue instead of a lease comp.

Can I use gift funds for the down payment?

Generally no. DSCR lenders typically require the down payment to come from the borrower’s own funds. Confirm with your lender before structuring the deal.

What credit score do I need for 80% LTV?

700 minimum through select lenders. Programs start at 620 with lower leverage.

Does down payment affect my rate?

Yes. More leverage typically means higher pricing. The trade-off between rate and capital deployment is worth running before you commit to a structure.

How many properties can I finance using DSCR?

There is no hard cap the way conventional financing has. Each property qualifies on its own performance. Portfolio size doesn’t disqualify you.

Run the Numbers Before You Go Under Contract

The down payment structure affects every deal you do from here forward.

Not just this one.

Investors who run the numbers before they go under contract know exactly how much capital they’re committing, what leverage they qualify for, and how the structure fits their next move.

Investors who wait until closing often discover those options after the structure is already set.

Run the numbers here before you commit:

https://www.dscrfinancing.com/dscr-loan-calculator/

Prefer Video Instead?

I recently talked through how today’s investors are financing deals outside traditional lending structures, including leverage strategy, capital deployment, and portfolio growth, during a Boise investor podcast discussion.

Watch here:

Financing Deals Outside Traditional Lending Structures

About The Author

Patrick Penner is an Idaho DSCR mortgage strategist specializing in investor financing, co-living properties, Airbnb financing, rural investment properties, and portfolio growth strategies. Through Coast2Coast Mortgage, he works with investors nationwide to structure financing around long-term scalability, leverage, and property performance.

Learn more about Patrick Penner:

https://www.dscrfinancing.com/about/

Learn more about DSCR loans in Idaho:

https://www.dscrfinancing.com/dscr-loans-idaho/