Co-Living & PadSplit DSCR Loans in Idaho: What Matters Before You Refinance

The investors who run into the most trouble with co-living and PadSplit deals in Idaho are not the ones who made mistakes on the purchase. They are the ones who executed the acquisition correctly, improved the property, filled the rooms, and then found out the refinance did not work the way they expected. The property was performing. The lender was not seeing it the same way.

That gap between operational success and refinance outcome is the part of this strategy that receives the least attention before closing, and the most frustration after it.

Co-living and PadSplit models can produce stronger cash flow than a standard single-tenant rental, particularly in Idaho markets like Nampa and Caldwell where price appreciation has made traditional rental yields harder to achieve. The income advantage is real. The financing path to access that income on the back end is more specific than most investors realize going in.

Why Refinance Is a Different Conversation

Purchase financing and refinance financing are related, but they are not identical decisions.

At the purchase stage, lenders focus heavily on the borrower profile, down payment, reserves, and the overall strength of the file. At refinance, the emphasis shifts toward current property performance, lease documentation, occupancy history, appraisal support, seasoning requirements, and whether the lender remains comfortable with the underlying income model.

That difference matters more in co-living and PadSplit deals than in standard rentals. A property that was straightforward to acquire may face more scrutiny when the investor wants to pull capital back out. For a closer look at how DSCR lenders differ on these deals and what to look for when evaluating them, you can read more here: https://www.dscrfinancing.com/padsplit-co-living-dscr-idaho/

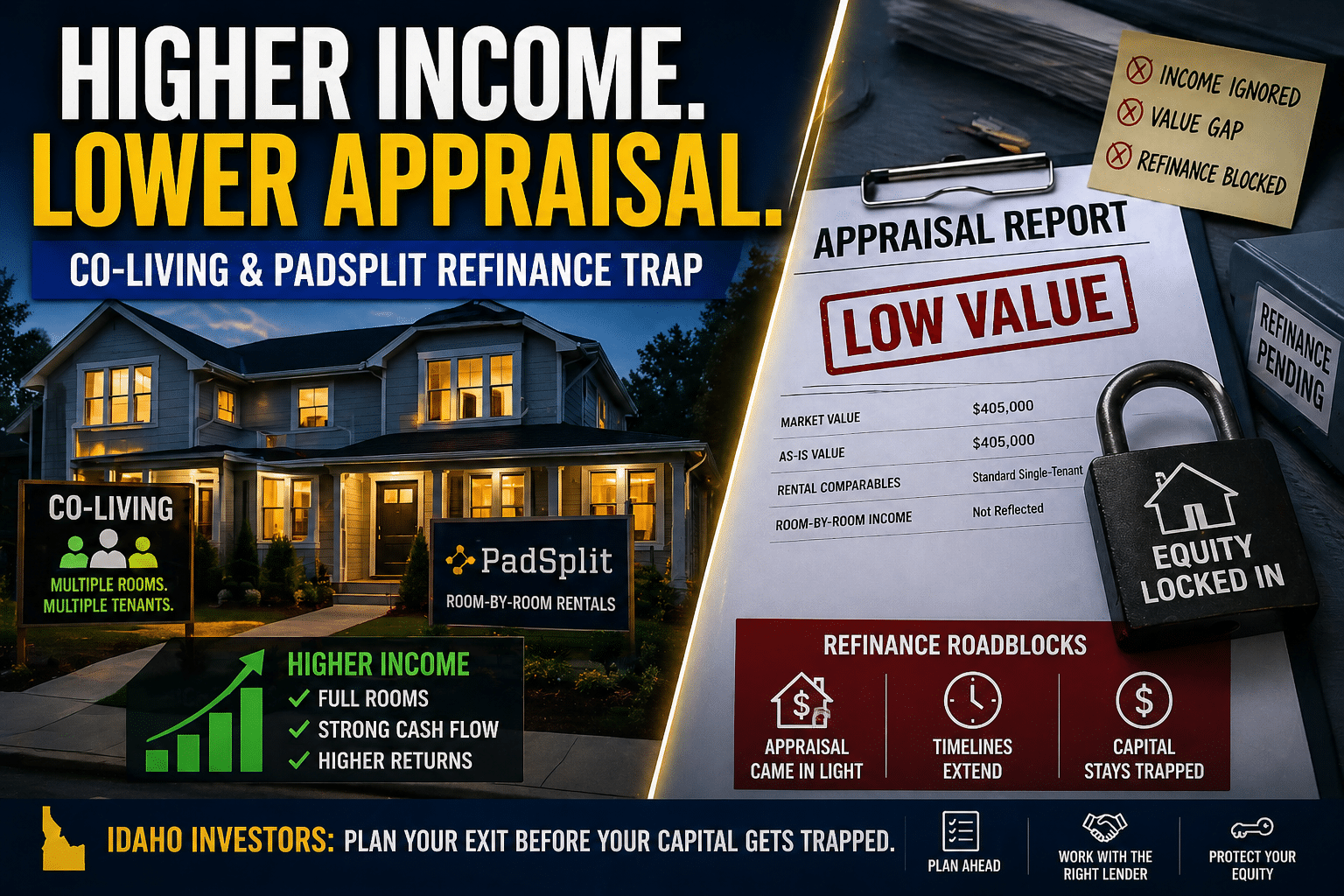

Why Higher Income Does Not Always Mean Higher Value

Many co-living and PadSplit properties produce more gross income than a traditional long-term rental. That improves cash flow and strengthens day-to-day performance. It does not always mean the appraisal will rise in the same proportion.

Appraisers rely on comparable sales, neighborhood data, and traditional rental benchmarks. In most Idaho markets, comparable sales for room-rental or co-living models are limited. A four-bedroom property operating as PadSplit in Boise or Meridian with four separate tenants is being valued against other four-bedroom properties rented to a single household or sitting vacant. Same beds, same baths, same square footage. The appraiser is not evaluating how many people are paying rent inside it or what the total income adds up to.

The result is a property that earns more but does not appraise higher because of it. An investor expecting to pull equity based on room-by-room revenue may find the appraisal reflects single-tenant assumptions instead. The refinance may still be possible, but the capital returned can be meaningfully lower than what the operating numbers suggested.

How Lenders View Room-by-Room Income

Not every lender evaluates room-rental income the same way, and the difference is more significant than most investors expect going in.

A lender who is comfortable with co-living and PadSplit income may accept aggregated room lease documentation, recognize the total income across all tenants, and underwrite the DSCR ratio based on what the property is actually producing. A lender who is not comfortable with this model may default to a single market rent figure from the appraisal, which reflects what the property would earn as a standard single-tenant rental. On a property generating $2,800 per month across four rooms where single-tenant market rent is $1,800, that difference alone can determine whether the loan qualifies and at what leverage.

Two lenders reviewing the same Idaho property can reach entirely different conclusions on qualifying income, available leverage, reserve requirements, and pricing, without either of them being wrong. They are simply operating under different guidelines. That is why lender fit often matters more in this space than rate, and why confirming that fit before the purchase closes is one of the most consequential decisions in the deal.

The Capital Trap Investors Miss

A common approach is to acquire the property, improve operations, increase income, and then refinance to recover capital for the next purchase. That can work well when the refinance assumptions were realistic from the start.

Problems arise when investors assume all lenders will treat the property the same way, assume the appraisal will mirror operational success, or assume cash-out timing will be straightforward. If lender options narrow, seasoning periods extend, or value comes in below expectations, capital stays tied up longer than planned. That delay can affect the next acquisition, reserve position, and overall growth timeline. Investors running a BRRRR strategy through co-living or PadSplit properties are particularly exposed to this dynamic. You can read more about how that refinance step is structured here: https://www.dscrfinancing.com/dscr-brrrr-strategy-idaho/

Why This Matters in Idaho

Across Boise, Meridian, Nampa, Caldwell, Twin Falls, and other growing Idaho markets, investors continue looking for ways to improve property performance and increase cash flow. Co-living and PadSplit models are part of that trend, particularly in markets where single-tenant cash flow has become harder to achieve at current price points.

Idaho investors benefit most when they underwrite both sides of the transaction before closing. Solving only the purchase side of the deal creates avoidable friction later, when capital is already committed and options are narrower.

What Experienced Investors Confirm Before They Buy

Before writing an offer on a co-living or PadSplit property, investors who execute consistently on these deals work through a specific set of questions. Which lenders are comfortable with this income model and how do they document it for underwriting? What valuation method is most likely to apply given the market and the comp base? How long before a cash-out refinance is realistic, and which lenders will participate in it? What happens to the plan if the original refinance assumptions change?

A short strategy conversation before the purchase can prevent months of friction after closing.

Frequently Asked Questions About Co-Living and PadSplit DSCR Loans in Idaho

Can you refinance a PadSplit property with a DSCR loan in Idaho?

Yes, through select lenders. The primary questions involve income documentation, property valuation, seasoning requirements, and whether the lender is comfortable with the operating model. Not every DSCR lender will engage with this property type, which makes lender selection on the front end directly relevant to what refinance options exist on the back end.

Do co-living properties appraise based on room-by-room income?

Not always. Many appraisals rely on comparable sales and market rent assumptions for the property type rather than the actual room-by-room revenue the property is generating. In most Idaho markets, limited comparable transactions for co-living or PadSplit properties mean appraisers default to conventional single-tenant data. That gap between operational income and appraised value is where many refinances come in below expectations.

Can room-by-room leases be used to qualify for a DSCR loan?

Some lenders will accept aggregated room lease documentation as qualifying income. Others will use a single market rent figure from the appraisal regardless of what the rooms are actually generating. This is highly lender specific and one of the most important variables to confirm before structuring the deal.

Is seasoning required before a cash-out refinance on a co-living property?

It depends on the lender and how the deal is structured. Some programs allow refinancing based on updated appraised value without a long seasoning period once the property is stabilized. Others require a holding period before new value can be used. Confirming the seasoning requirement with the lender before the acquisition closes is part of planning the exit accurately.

Should the refinance be planned before the purchase?

Yes. For co-living and PadSplit deals specifically, the refinance path needs to be part of the acquisition conversation. The income model, the carry period, the appraisal approach, and the lender’s guidelines on this property type all connect directly to whether the exit performs the way the deal was underwritten.

What if the deal is already closed and the refinance is not working as expected?

This is a common situation and it is not necessarily a dead end. The first step is understanding why the refinance is not working, whether it is a valuation issue, an income documentation issue, a lender overlay, or a seasoning requirement. Different lenders approach these deals differently, and a file that was declined or came in below expectations with one lender may still have viable paths through another. A strategy conversation focused specifically on the refinance side is usually the right starting point.

Final Thought

Many investors underwrite the purchase carefully and give limited attention to the refinance. Experienced investors evaluate both. Getting into the property matters, but preserving options after closing often matters just as much. For co-living and PadSplit deals in Idaho, those two conversations need to happen at the same time.

If you are evaluating a co-living or PadSplit property in Idaho and want to understand realistic DSCR financing options before committing, you can start here: https://www.dscrfinancing.com/dscr-loans-idaho/

To run numbers before the conversation, the DSCR calculator is here: https://www.dscrfinancing.com/dscr-calculator/

About The Author

Patrick Penner is an Idaho DSCR mortgage strategist specializing in investor financing, co-living properties, Airbnb financing, rural investment properties, and portfolio growth strategies. Through Coast2Coast Mortgage, he works with investors nationwide to structure financing around long-term scalability, leverage, and property performance.

Learn more: