BRRRR Refinance Idaho: Why Investors Get Stuck After the Rehab

Most investors think the hard part of a BRRRR deal is the rehab. Finding the property, managing contractors, staying on budget, and getting the work done on schedule absorb almost all of the attention. Once the project wraps, the assumption is that the easy part begins. The refinance pulls the capital back out, and that capital funds the next acquisition.

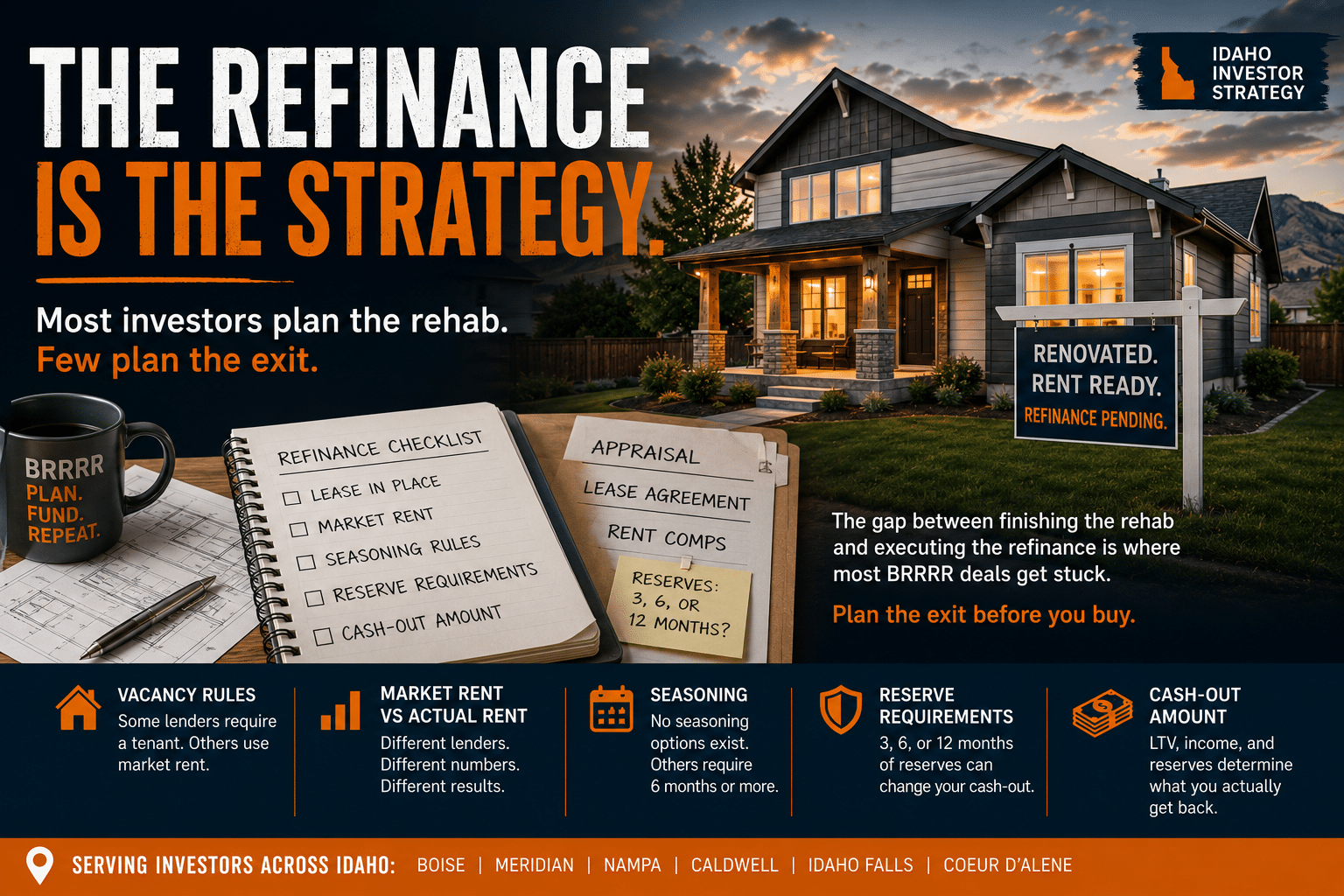

In practice, the refinance is where a surprising number of Idaho BRRRR investors get stuck, and it almost never happens for the reason they expect. The rehab did not fail, and the property really is worth more than they paid for it. The problem is that they never found out what the refinance lender would actually require before they started spending money. The gap between finishing the project and executing the refinance is where most BRRRR strategies slow down, and it is almost always a planning problem rather than a property problem. The same pattern shows up on deals in Boise, Meridian, Nampa, Caldwell, Idaho Falls, and Coeur d’Alene every year.

This article is about that gap. If you want the full range of investor financing in the state first, the DSCR loans in Idaho pillar covers it, but the focus here is the one step most investors underplan: the exit.

DSCR loans in Idaho:

https://www.dscrfinancing.com/dscr-loans-idaho/

Most Investors Plan the Rehab. Few Plan the Refinance.

The BRRRR strategy looks simple on paper. You buy, rehab, rent, refinance, and repeat. Most of the attention lands on the first three steps, where investors analyze acquisition costs, estimate renovation budgets, and study after-repair values in detail. The refinance gets treated as a formality, something that happens on its own once the hard work is done.

It is not automatic. A property can be fully renovated, rentable, and worth significantly more than the purchase price and still hit serious friction the moment the refinance begins. The issue is rarely the property itself. It is how the next lender evaluates everything that comes after the rehab, and that evaluation looks nothing like the investor’s own view of the deal.

BRRRR strategy:

https://www.dscrfinancing.com/brrrr-dscr-loans-idaho/

What the Refinance Lender Is Actually Looking At

The investor and the refinance lender are not looking at the same thing. The investor sees completed renovations, increased value, and the next acquisition waiting on the other side. The lender is asking a different set of questions entirely: is the property leased, how is rental income being calculated, does the deal meet seasoning requirements, what reserves are required at closing, and will market rent support the debt.

Consider a Nampa investor who recently finished a full renovation on a single-family property. The purchase price was 210,000 dollars, the rehab came in at 38,000 dollars, and the after-repair value appraised at 315,000 dollars. On paper, that is a textbook BRRRR. The refinance stalled anyway, because the property was not leased yet and the lender required an executed lease before it would proceed. The investor lost six weeks waiting for a tenant, and the next deal slipped. Nothing about the property changed during those six weeks. The lender’s requirements were simply different from what the investor had assumed.

Vacancy Catches BRRRR Investors Off Guard

The rehab finishes, the photos are done, and marketing has started, so the investor assumes the refinance can move forward. Some lenders agree and will move ahead. Others require a tenant in place before they will close. That single difference in lender approach can cost weeks or months depending on how quickly the unit leases, and in a slower leasing season it can push the refinance into an entirely different rate environment.

This is the same dynamic that decides ordinary purchase approvals, where one lender will not touch a vacant unit while another underwrites it on the appraiser’s market rent. It is worth understanding why one lender approves what another declines, because in a BRRRR strategy lender selection matters as much as property selection. The property does not change. The lender’s vacancy policy does.

Why one lender approves what another declines:

https://www.dscrfinancing.com/dscr-loan-denied-idaho/

Market Rent Versus Actual Rent, and Which Number the Lender Uses

Some lenders qualify the refinance using the market rent figure from the appraisal. Others require an executed lease and will use only that number. The difference can materially change the DSCR calculation and, with it, how much cash actually comes back out of the deal.

Picture a Caldwell property with a signed lease at 1,450 dollars a month and an appraisal that pegs market rent at 1,900 dollars. Those two figures produce two completely different refinance outcomes depending on which one the lender’s guidelines tell it to use. Same property. Same renovation. Same appraisal. Different lender, different outcome. An investor who does not know which figure the refinance lender will use before the rehab begins is making a capital decision without all of the information, and on a BRRRR deal that decision drives the entire return.

Market rent versus actual rent:

https://www.dscrfinancing.com/market-rent-vs-actual-rent-dscr-loans-idaho/

The Seasoning Assumption

Most investors assume they have to wait six months before they can refinance. Sometimes that is true, and sometimes it is not. Certain DSCR lenders offer no-seasoning programs that let you refinance against the new appraised value soon after the work is done, generally up to 80 percent loan to value on a long-term rental. Other lenders require a longer holding period before that new value can be used in underwriting, and a short-term rental still needs roughly six months of seasoning before any cash-out is on the table. The mechanics of that timeline are covered in the no-seasoning cash-out refinance guide.

The difference between those approaches determines how quickly capital returns to you and whether the next acquisition happens this year or next. On a 315,000 dollar after-repair value at 80 percent loan to value, that is roughly 252,000 dollars to refinance against. Getting that capital back in month two instead of month eight changes the pace of the entire portfolio, which is why seasoning is a question to answer before the rehab, not after.

No-seasoning cash-out refinance guide:

https://www.dscrfinancing.com/dscr-no-seasoning-cash-out-refinance-idaho/

Reserve Requirements at Closing

This one catches investors off guard more than almost anything else. Depending on the property, the loan amount, and the size of the overall portfolio, some lenders require three, six, or even twelve months of reserves at closing. The investor spends months planning the acquisition, managing the rehab, and calculating the refinance proceeds, and then the approval arrives with a reserve requirement nobody planned for.

Imagine an investor expecting to pull 70,000 dollars out of a refinance to fund the next deal. The refinance gets approved, the appraisal lands where expected, and the cash-out works on paper. Then the lender requires six months of reserves across several financed properties, and a meaningful portion of the capital that was supposed to move into the next acquisition never makes it there. Nothing actually went wrong with the deal. The investor planned the rehab and never planned the refinance. That is exactly why experienced BRRRR investors look at reserve requirements before the project starts rather than discovering them at the closing table.

How Experienced Investors Structure the Refinance First

The investors who execute BRRRR strategies consistently in Idaho are not smarter about renovations. They are smarter about the refinance. Before the first dollar of rehab money is spent, they already know how the future lender handles vacancy, how rental income will be calculated, whether seasoning applies and for how long, what reserves will be required at closing, and how much cash-out is realistic at the appraised value. That clarity changes how the entire project is structured, because the rehab becomes one part of a financing strategy rather than an isolated construction project with a vague plan for what comes next.

It is also why working with someone who places loans with more than one lender matters more than the rate on any single quote. A good originator already knows which desk will close on a vacant unit, which one uses market rent, and which one offers a no-seasoning option, and that knowledge is what keeps the timeline intact. If you want a sense of how Idaho investors weigh those options, the DSCR lenders in Idaho page is a useful starting point.

DSCR lenders in Idaho page:

https://www.dscrfinancing.com/dscr-lenders-idaho/

The Refinance Is the Strategy

Most investors believe the rehab creates the return. The refinance is what determines whether the strategy repeats. A well-executed rehab paired with a poorly structured refinance does not recycle capital. It traps it. The next acquisition gets delayed, the portfolio slows, and the investor who planned everything except the exit ends up waiting for equity to build the slow way.

That is why the strongest BRRRR projects in Idaho do not start with the property. They start with the exit. If you are evaluating a deal in Nampa, Caldwell, Meridian, Boise, or Idaho Falls and you want to understand how the refinance will be structured before you commit to the acquisition, the smartest move is a quick strategy call up front. You can start from the Idaho investment property loans overview and book a strategy call so the financing and the rehab are built together rather than in sequence.

Idaho investment property loans overview:

https://www.dscrfinancing.com/idaho-investment-property-loans/

Frequently Asked Questions

Can I refinance a BRRRR property in Idaho before six months?

Sometimes, yes. While many investors assume a six-month seasoning period is mandatory, certain DSCR lenders offer no-seasoning programs that let you refinance against the new appraised value soon after the rehab is complete, generally up to 80 percent loan to value on a long-term rental. Other lenders do require a longer holding period before the new value can be used, so the answer depends entirely on which lender you place the loan with. Confirming the seasoning rule before you start the project is the only way to plan the timeline accurately.

Does my BRRRR property need to be leased before I can refinance?

It depends on the lender. Some lenders will close the refinance using the appraiser’s market rent even when the unit is still vacant, while others require an executed lease before they will proceed. If your refinance is being held up because the property is not leased, that is a single lender’s policy rather than a universal rule, and a different lender may be able to move forward on market rent. This is one of the most common reasons a BRRRR refinance stalls when the investor expected it to be routine.

How much cash can I pull out of a BRRRR refinance in Idaho?

That is driven by the appraised value and the lender’s loan-to-value limit. As a general example, a long-term rental refinanced at 75 percent loan to value on a 315,000 dollar appraisal allows roughly 236,000 dollars of debt to refinance against, and seasoned cash-out programs can reach higher with the right profile. The actual cash in hand also depends on your existing loan balance and any reserve requirements the lender applies at closing, so the headline loan-to-value is only part of the picture.

Why is the amount I can refinance different from my appraised value?

Because lenders lend a percentage of value, not the full value, and because the income side of the deal has to support the loan. The appraisal sets the value, but the loan-to-value cap, the DSCR calculation, and the lender’s reserve requirements all reduce the amount that actually reaches you. Two lenders looking at the identical appraisal can land on different numbers depending on whether they use market rent or the signed lease and how much they hold back in reserves.

What reserves do I need for a DSCR refinance?

Reserve requirements vary by lender and are influenced by the property, the loan amount, and the size of your overall portfolio. Some lenders ask for three months of payments, while others want six or twelve, and the requirement can be applied across multiple financed properties rather than just the subject property. Because reserves can absorb a large share of your expected cash-out, it is worth confirming the requirement before the rehab begins so the number does not surprise you at closing.

About The Author

Patrick Penner is an Idaho DSCR mortgage strategist specializing in investor financing, co-living properties, Airbnb financing, rural investment properties, and portfolio growth strategies. Through Coast2Coast Mortgage, he works with investors nationwide to structure financing around long-term scalability, leverage, and property performance.

Learn more about Patrick Penner: https://www.dscrfinancing.com/about/

Learn more about DSCR loans in Idaho: https://www.dscrfinancing.com/dscr-loans-idaho/