Why Some DSCR Loans Hit Your Personal Credit and Others Don’t

Most investors think if they close a DSCR loan in an LLC, it automatically stays off their personal credit.

That assumption costs people later.

Because not all DSCR lenders handle these loans the same way.

Some structure investor loans through true business-purpose lending platforms.

Others run DSCR through broader Non-QM systems that may produce different reporting outcomes depending on servicing and where the loan goes after closing.

That difference can affect the next approval more than this one.

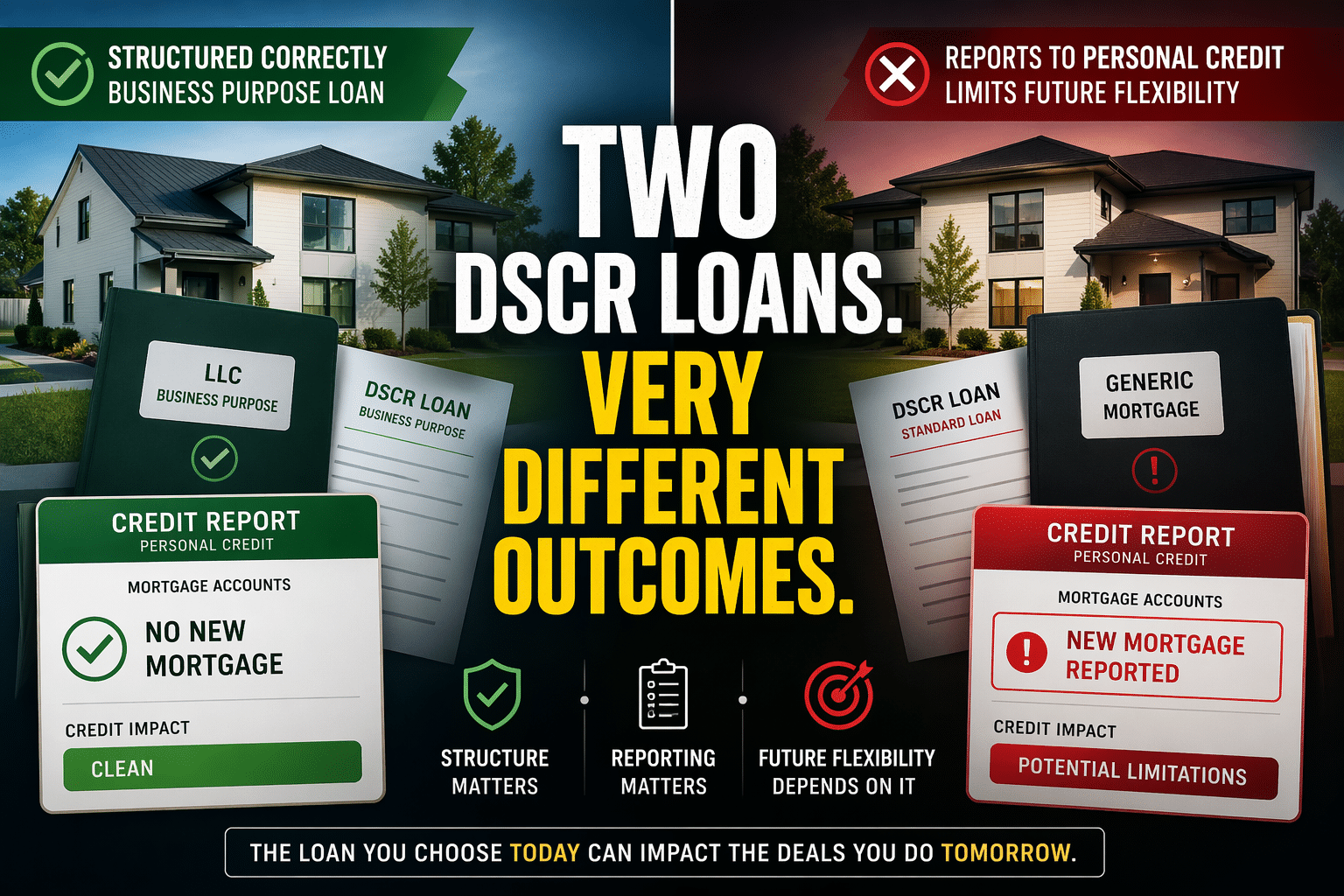

The loan you choose today can compete with the loan you need tomorrow.

Not All DSCR Lenders Are the Same

Many investors shop DSCR loans by rate, points, or leverage.

Those matter.

But lender structure matters too.

Some lenders specialize in investment-property lending only.

No owner-occupied loans. No consumer mortgage focus.

Others offer DSCR as one product alongside bank statement loans, no-ratio products, and primary residence lending.

That backend difference often shows up later in servicing, reporting, and future financing flexibility.

LLC Vesting Does Not Remove the Personal Guarantee

One point investors should understand early:

These are not non-recourse loans.

Even when a DSCR loan closes in an LLC, lenders typically still require a personal guarantee.

That means the LLC may hold title and be the borrowing entity, but the guarantor still matters.

So the real question is usually not whether there is a guarantee.

The real question is how the loan is structured, serviced, and whether it reports to personal credit.

True Investor Lenders vs General Non-QM Platforms

This is where lender type matters.

Many true investor-focused lenders only lend on investment properties.

They do not originate owner-occupied mortgages.

Their systems are built around business-purpose lending.

In many cases, loans structured this way do not report to personal credit as long as the loan remains current and does not become delinquent.

That can be a major advantage for investors planning future purchases.

General Non-QM lenders can be different.

Many offer DSCR loans alongside owner-occupied, bank statement loans, no-ratio products, and other consumer-oriented financing.

Some broader lenders also entered the DSCR space as demand expanded after building their core business around conventional, FHA, VA, and other owner-occupied lending.

That does not make them bad lenders.

But it can mean their systems, servicing practices, and investor-loan treatment may differ from lenders built exclusively for business-purpose investment lending.

Because of that mixed platform, reporting outcomes may not always be the same.

Sometimes it depends on how the loan is boarded, who services it later, and what happens after the loan is sold.

That is why two DSCR loans can look similar at closing but behave differently later.

The Tradeoff Many Investors Miss

This is where strategy matters.

A true business-purpose lender that typically does not report to personal credit can be a strong option when the deal fits their box.

But not every deal fits that box.

Sometimes a broader Non-QM lender may allow something the investor-only lender will not.

Different DSCR ratios.

Different reserve requirements.

Different property types.

Different lease treatment.

Different rural guidelines.

Different seasoning rules.

That can mean the lender most attractive on future credit flexibility is not always the lender that can close the loan today.

And the lender that can close today may come with a future tradeoff.

That is why serious investors compare more than one variable.

The right move is not always the cleanest structure.

Sometimes it is the structure that gets you into the right asset now with eyes open to the future tradeoff.

Why Servicing Transfers Matter

Many DSCR loans are sold or transferred after closing.

That is normal.

What changes is the next servicer may not handle reporting the same way the original lender did.

That is where confusion can happen.

A loan that was expected to stay off personal credit may later appear due to coding, servicing setup, or transfer handling.

Investors should monitor credit after transfers instead of assuming the original structure remains unchanged.

The W-9 and LLC Documentation Signal

Sometimes the paperwork tells the story.

When a lender requires a W-9 tied to the LLC, EIN documentation, business-purpose affidavits, and closes with LLC vesting, that often signals a stronger business-purpose structure.

It does not override every scenario.

But if reporting issues later arise, those documents can become important support when disputing inaccurate consumer credit reporting.

If It Reports Incorrectly

Handle it quickly.

- Pull all three credit reports

- Gather closing documents, guarantee documents, W-9, and LLC paperwork

- Contact the servicer first and request correction or explanation

- File bureau disputes when appropriate

- Reference Fair Credit Reporting Act rights if inaccurate data is being furnished

- Keep records of all communication

Problems ignored often stay unresolved.

Problems addressed early are usually easier to fix.

Why Self-Employed Investors Should Care More

This can matter even more for self-employed borrowers.

Heavy write-offs already compress taxable income.

Future conventional or income-based approvals may already be tighter.

So preserving personal credit flexibility can matter more than shaving a small amount off rate today.

Sometimes the hidden cost of a loan is not pricing.

It is reduced options later.

What This Means for Idaho Investors

Whether you are buying in Boise, Meridian, Nampa, Caldwell, Twin Falls, or scaling across multiple states, the wrong lender can quietly slow portfolio growth.

The right lender can help preserve flexibility for the next purchase, especially when you have access to 200+ lending options.

That matters when you plan to keep building.

What Smart Investors Ask Before Closing

Before choosing a DSCR lender, ask:

- Is this lender built only for investors or does it also originate owner-occupied loans?

- How is this loan commonly structured and serviced?

- Will this loan typically report to personal credit?

- Is the borrower my LLC or me personally?

- How could this affect my next approval?

- Is this the best lender for my long-term plan?

Those questions can matter more than a small pricing difference.

Final Thought

Most investors compare rates.

Smart investors compare what happens after closing.

How it reports.

How it transfers.

How it affects the next purchase.

Because the wrong loan rarely feels wrong on day one.

It shows up later.

Next Steps

Before choosing a DSCR lender, compare more than rate.

Compare how the loan is structured.

Compare how it may be serviced later.

Compare whether it helps or hurts your next move.

Run the numbers on our DSCR calculator.

Or message CREDIT REPORT for a quick 15-minute strategy review.