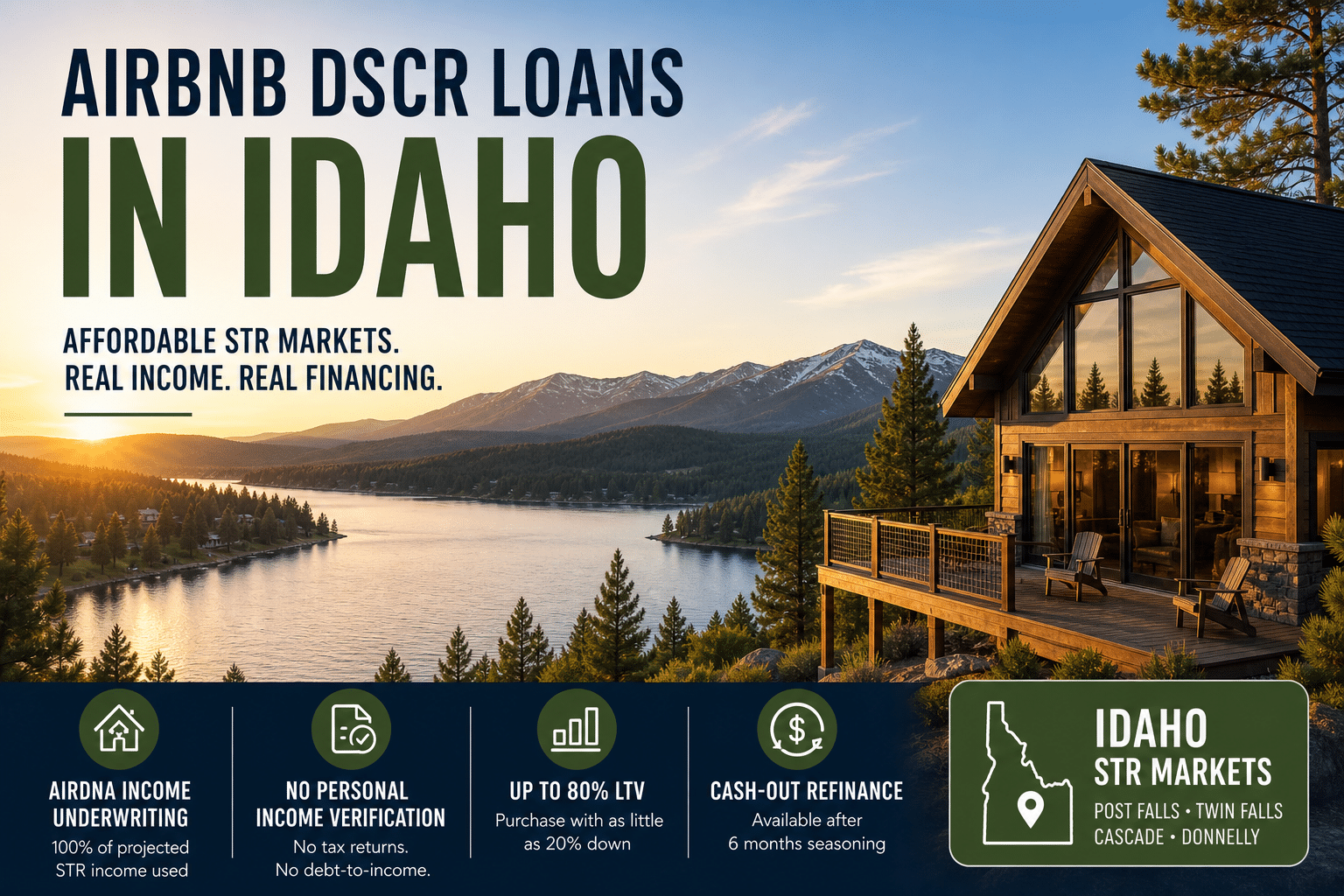

AIRbnb DSCR Loans in Idaho: Affordable STR Markets in Post Falls, Twin Falls, Cascade & Donnelly

Idaho’s short-term rental market isn’t just Coeur d’Alene and Sun Valley.

Those markets get the attention. But the investors finding the strongest returns right now are looking at something different.

Markets where entry prices don’t require a seven-figure down payment. Markets where tourism demand is real and growing. Markets where the DSCR math actually works.

Post Falls. Twin Falls. Cascade. Donnelly.

Four Idaho STR markets inside the $400,000 to $700,000 purchase range, with financing structures built specifically for how these properties perform.

For investors already evaluating the premium Idaho STR markets, that breakdown is here: https://www.dscrfinancing.com/dscr-loans-idaho/

Why Most Investors Overlook These Markets

The conversation about Idaho vacation rental financing defaults to the obvious names.

McCall. Sandpoint. Sun Valley.

Those are real markets with real demand. But they’re also $800,000 to $1,150,000 entry points. The down payment alone filters out most investors before financing even comes into the conversation.

The markets covered here produce genuine STR income at purchase prices where DSCR financing creates real leverage. Not just theoretically, but in the actual numbers.

That’s the difference.

What Airbnb DSCR Loans Do for These Markets

Conventional lenders underwrite STR properties using long-term lease comps.

What would this property rent for on a twelve-month lease? That’s the number they use.

In Post Falls, Twin Falls, Cascade, and Donnelly, markets where Airbnb income meaningfully exceeds long-term rental rates, that approach kills deals that should close.

DSCR loans use 100% of AirDNA projected short-term rental income.

No discount. No substitution. No converting a vacation rental into something it isn’t.

Combined with 80% LTV on single family STR purchases, no personal income verification, and cash-out refinances available after six months seasoning, this is where the accessible market story gets interesting.

The Four Markets

Post Falls

Median purchase price: approximately $539,000.

AirDNA annual revenue: approximately $48,500.

Post Falls sits fifteen minutes from Coeur d’Alene. It’s absorbing overflow tourism from one of Idaho’s strongest STR markets while offering entry prices that Coeur d’Alene hasn’t seen in years.

That dynamic is showing up in the data. Gross STR revenue in Post Falls jumped roughly 100% from 2023 to 2024. That’s not a mature market leveling off. That’s a market still finding its ceiling.

Non-rural designation. Strongest growth trajectory of any market on this list.

80% LTV on a $539,000 purchase requires $107,800 down. Conventional financing at 25% down requires $134,750.

Capital difference: $26,950.

Twin Falls

Median purchase price: approximately $385,000.

AirDNA annual revenue: approximately $36,000 to $45,000 depending on property.

Twin Falls is the most accessible STR entry point in Idaho.

Shoshone Falls drives year-round tourism in a way most Idaho markets can’t claim. Outdoor recreation, climbing, events. Demand here doesn’t compress into a single season the way mountain markets do.

For investors who want strong STR income without the premium market price tag, Twin Falls is the clearest path.

80% LTV on a $385,000 purchase requires $77,000 down. Conventional financing at 25% down requires $96,250.

Capital difference: $19,250.

Cascade

Median purchase price: approximately $520,000.

AirDNA annual revenue: approximately $41,000 to $60,000 depending on property.

Cascade sits between Boise and McCall. That position matters.

It captures McCall overflow while offering purchase prices that McCall stopped producing years ago. Outdoor recreation, skiing, lake access, hiking, snowmobiling, anchors demand across multiple seasons.

Top performing properties in Cascade are clearing $5,000 per month. Low regulation environment. Growing inventory of STR-quality properties still priced within reach.

80% LTV on a $520,000 purchase requires $104,000 down. Conventional financing at 25% down requires $130,000.

Capital difference: $26,000.

Donnelly

Median purchase price: approximately $680,000.

AirDNA annual revenue: approximately $40,000 to $64,000 depending on property.

Donnelly is the highest entry point on this list, but it belongs here.

Tamarack Resort is the anchor. Winter ski demand combined with summer lake and outdoor recreation activity produces a two-season STR market that most accessible price-point locations can’t match.

Strong performers are clearing $5,357 per month. The market is still underdiscovered relative to what Tamarack’s continued growth is going to do to STR demand over the next few years.

80% LTV on a $680,000 purchase requires $136,000 down. Conventional financing at 25% down requires $170,000.

Capital difference: $34,000.

The Three DSCR Differentiators That Matter in These Markets

AirDNA Income Underwriting

100% of projected STR income is used. No discount.

In markets like Post Falls, Twin Falls, Cascade, and Donnelly where the gap between long-term lease rates and Airbnb income is significant, this shift alone determines whether a deal qualifies.

No Personal Income Verification

No W2s. No tax returns. No debt-to-income calculation.

The property qualifies on its own performance. Self-employed borrowers, investors with large depreciation positions, and anyone already carrying multiple financed properties. None of that disqualifies you here.

LTV and Refinance Structure

80% LTV on single family STR purchases with a 700 minimum credit score.

Cash-out refinances available after six months seasoning. 75% LTV at 660 credit score. 80% LTV through select lenders at 700.

Rural Designation Matters in These Markets

Cascade and Donnelly are likely rural-designated markets. Rural designation affects which lenders will finance the deal and what programs are available.

Confirming rural classification before structuring the deal is critical. Not after.

More on rural DSCR loans in Idaho here: https://www.dscrfinancing.com/rural-dscr-loans-idaho/

How the Process Works

Before you go under contract, AirDNA projections are run for the property.

You can also run your own scenario first using our DSCR calculator:

https://www.dscrfinancing.com/dscr-calculator

You see:

- Projected revenue

- DSCR

- LTV options

- Rural designation

Once under contract: appraisal is ordered, DSCR is confirmed, underwriting focuses on the property. No personal income documentation required.

Closings typically happen in 21 to 30 days. LLC vesting is allowed.

Frequently Asked Questions

Do these markets qualify for Airbnb DSCR loans? Yes. Post Falls, Twin Falls, Cascade, and Donnelly all qualify. Rural designation varies by lender and affects which programs are available. Confirm that before you structure the deal.

What credit score is required? Programs start at 620. Maximum leverage requires 700. Best pricing starts at 720. Where you land on that range affects your options more than most borrowers expect.

Can I finance under an LLC? Yes. LLC vesting is allowed and common for investors building portfolios.

Is personal income verified? No. The property qualifies on its own projected income. Your W2s and tax returns stay out of it entirely.

What is the maximum LTV? 80% LTV on single family STR purchases with a 700 minimum credit score. Lower credit profiles have options. They just come with different leverage.

How long does closing take? 21 to 30 days typically. File strength and lender matter.

The Accessible Market Advantage

The premium Idaho STR markets get the headlines.

But the deal that actually works, the one where the down payment is manageable, the DSCR math clears cleanly, and there’s still room for the market to grow, that deal is more likely to be in Post Falls or Cascade than Sun Valley.

Most investors never look here. That’s the advantage.

Run the numbers on your property before you go under contract: DSCR Calculator