DSCR Loans in Idaho: Why Financing Strategy Now Determines Whether Deals Close

Idaho investors are not struggling because opportunities disappeared.

They are struggling because financing assumptions have not kept pace with how the market now behaves.

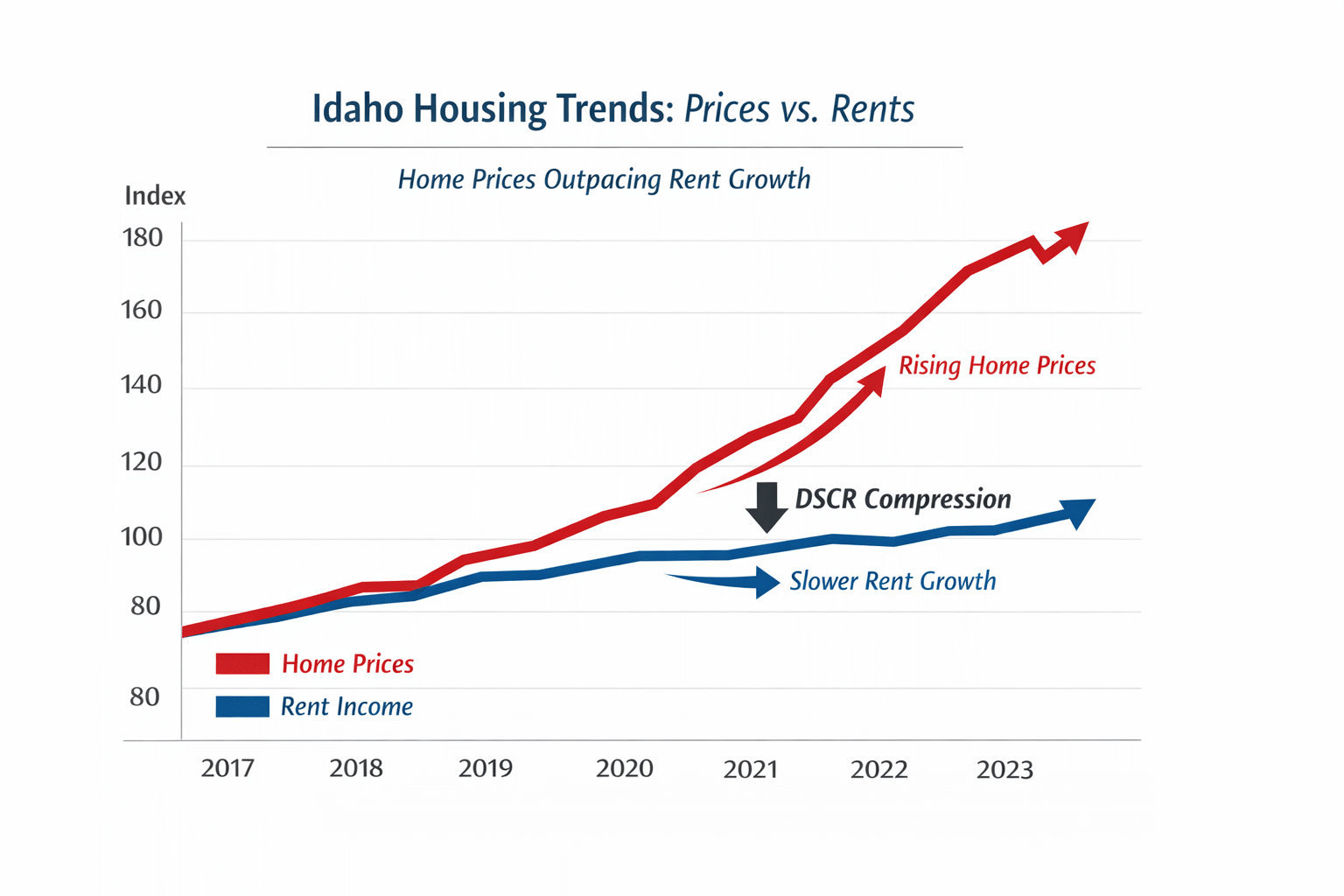

Property values in many areas — especially across the Treasure Valley — have risen faster than achievable rental income. In contrast, secondary and rural markets throughout Idaho continue to support stronger debt service coverage ratios.

This divergence has changed how DSCR loans function in practice.

Transactions that would have easily qualified several years ago now require a more precise approach to capital structuring. Understanding lender interpretation, property income dynamics, and refinance positioning has become central to whether an acquisition proceeds or stalls.

DSCR lending remains one of the most scalable financing tools available to Idaho investors. But its effectiveness increasingly depends on how intelligently it is applied.

Coverage Ratios Are No Longer a Simple Pass-Fail Metric

Debt service coverage ratios in Idaho now range across a much wider spectrum than most investors realize.

Traditional DSCR transactions may require coverage near or above 1.0. However, approvals can occur at significantly lower thresholds when property performance characteristics, borrower strength, and capital contribution align with lender risk models. In certain scenarios, no-ratio DSCR structures are viable, particularly for specialized income-producing assets such as care homes or unique rental configurations.

This flexibility is not uniform across lenders.

The outcome of a DSCR application often depends less on the property itself and more on which underwriting framework is applied.

Rent Compression Is Driving Financing Complexity

The Treasure Valley illustrates the primary challenge.

Acquisition pricing in Boise and surrounding submarkets has escalated rapidly, while rent growth has progressed at a slower pace. This compresses coverage ratios and forces investors to reconsider how they structure leverage.

In contrast, markets outside core metropolitan areas frequently maintain stronger rent-to-value relationships. Rural Idaho, workforce-driven cities, and smaller metropolitan zones continue to provide DSCR profiles that support higher leverage levels.

This geographic divergence requires lender selection that reflects local performance patterns rather than generalized statewide assumptions.

Property Strategy Is Reshaping DSCR Demand

Investor behavior across Idaho is evolving.

Traditional long-term rental acquisitions remain foundational, but emerging strategies now influence financing requirements. BRRRR transactions, short-term rentals, co-living models, and room-based income structures are becoming more prevalent as investors adapt to affordability pressures and shifting tenant demand.

Short-term rental financing has expanded particularly quickly. Higher leverage thresholds on purchase transactions and refinance structures allow investors to pursue opportunities in tourism-driven markets where conventional underwriting may impose constraints.

Similarly, rural properties and manufactured homes on permanent foundations are increasingly relevant components of investor portfolios. Financing availability for these asset types depends heavily on lender familiarity with localized risk profiles.

Misconceptions Continue to Limit Investor Growth

A significant portion of DSCR friction in Idaho stems from investor assumptions rather than lender restrictions.

Many investors remain unaware that qualification can occur without reliance on personal or business income. Others assume scaling a portfolio will eventually require transitioning back to conventional underwriting. Down payment verification requirements, credit scoring treatment for LLC vesting, and documentation expectations are frequently misunderstood.

First-time investors often believe DSCR financing is reserved for experienced operators. In practice, eligibility depends more on asset performance and borrower profile than on portfolio size.

Clarifying these misconceptions expands access to capital and accelerates acquisition timelines.

Refinance Strategy Must Be Considered at Acquisition

Another recurring challenge involves post-rehab capital recovery.

Investors frequently assume that refinancing to capture new value requires extended seasoning periods. In reality, certain DSCR structures allow earlier recognition of stabilized performance when lender guidelines and appraisal methodology align.

Misalignment between renovation assumptions and refinance planning can restrict liquidity even when property income improves. This reinforces the importance of structuring exit pathways before acquisition rather than retroactively adjusting financing strategy.

Appraisal Interpretation Remains a Key Constraint

Income optimization strategies do not automatically translate into valuation outcomes.

Attempts to increase property value based solely on room count or operational configuration often encounter resistance when comparable sales do not reflect similar structures. Appraisers typically anchor valuation to market evidence rather than projected income models.

Understanding how appraisal methodology interacts with DSCR underwriting prevents unrealistic refinance expectations and supports more predictable capital outcomes.

DSCR Lending Across Idaho’s Diverse Markets

Idaho functions as a collection of distinct lending environments.

Urban markets exhibit tighter coverage ratios but strong long-term appreciation dynamics. Rural regions frequently support higher leverage due to favorable rent-to-price relationships. Tourism-driven zones introduce seasonal income considerations that influence underwriting.

Financing strategies that succeed statewide account for these differences.

DSCR loans continue to provide scalable capital access across single-family rentals, short-term accommodations, manufactured housing, and specialized income properties. The effectiveness of this access depends on aligning lender selection with market-specific performance characteristics.

Financing Outcomes Now Reflect Structuring Intelligence

As Idaho’s investment landscape matures, financing decisions increasingly shape portfolio trajectories.

Coverage ratios, appraisal interpretation, refinance timing, and lender risk tolerance collectively determine whether capital remains accessible as investors scale.

DSCR lending remains central to this process. However, its impact is no longer defined solely by product availability. It is defined by how effectively financing frameworks adapt to evolving market conditions.

Investors who recognize this shift are better positioned to continue acquiring assets despite changing valuation dynamics.