Market Rent vs Lease Rent in DSCR Loans in Idaho: Why the Number Used Determines the Outcome

On almost every DSCR loan, two different rent figures exist at the same time. One comes from the lease. The other comes from the appraisal. The outcome of the deal depends on which one the lender chooses to use.

Most investors do not think about this distinction until the refinance is already in motion. By that point, the deal is already structured around a number the lender may not recognize. That gap between expected income and recognized income is where refinances stall, capital stays stuck, and BRRRR timelines extend past what was planned.

Where Lease Rent and Market Rent Come From

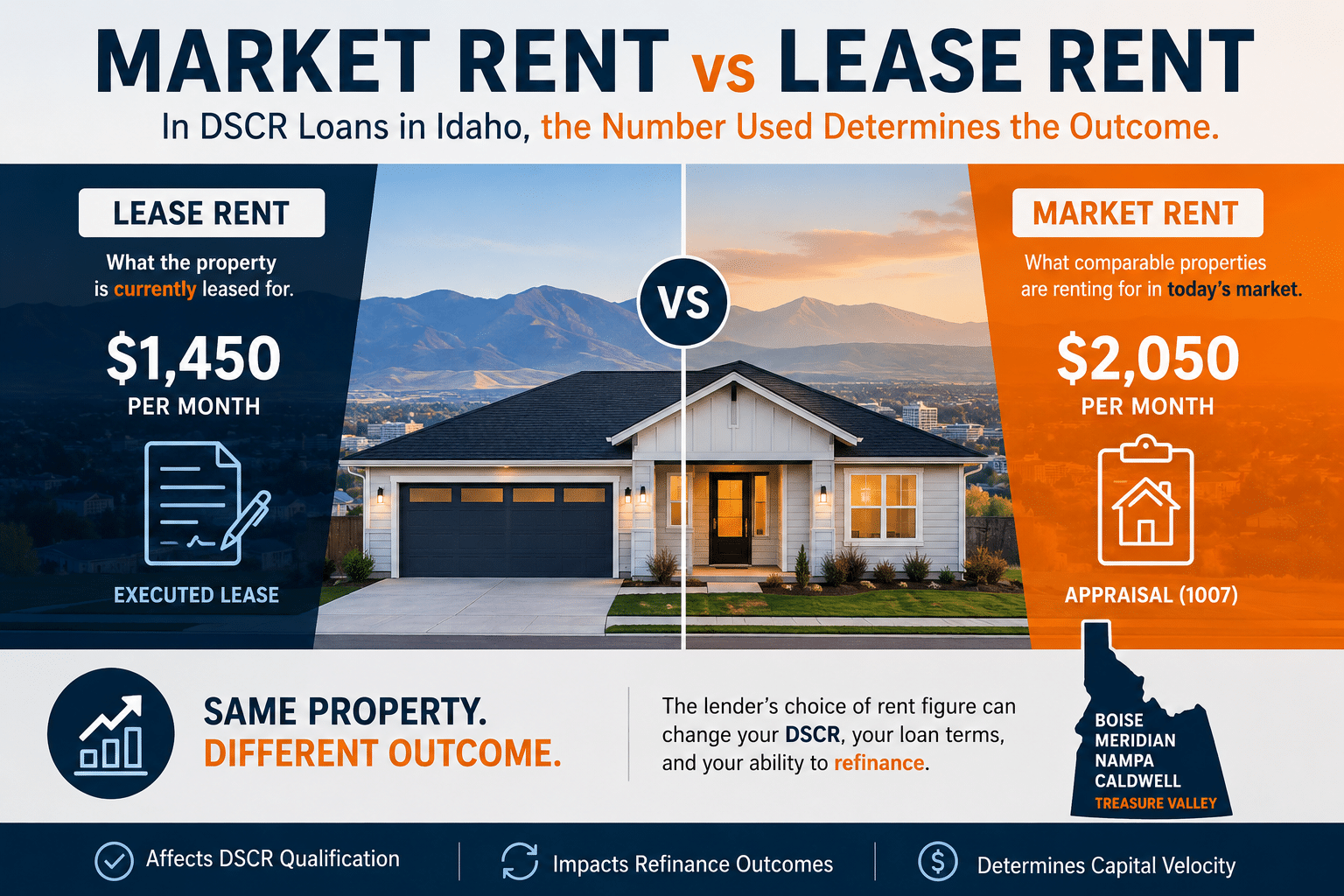

Lease rent is the amount the tenant is currently paying under an executed lease agreement. It is what the property is actually producing today.

Market rent comes from the appraisal, typically documented on the 1007 rent schedule. It represents what comparable properties are expected to rent for in the current market, regardless of what the subject property is leased at.

These two numbers are often not the same. In many Idaho markets, especially across Boise, Meridian, Nampa, and Caldwell, that gap has widened over the last several years. Properties with long-term tenants, recently renovated units, or below-market leases frequently show a meaningful difference between what the property is producing and what it could produce.

How This Changes DSCR Loan Qualification

DSCR loans qualify based on income relative to the monthly debt obligation. If the lender uses lease rent, the qualification reflects what the property is currently producing. If they use market rent, it reflects what the property could produce under current market conditions.

A small difference in rent can materially change the DSCR ratio and, with it, the outcome of the loan.

A property renting at $1,450 with a projected market rent of $2,050 may fall below a 1.0 DSCR using the lease figure, but exceed that threshold using market rent. That shift affects loan eligibility, available leverage, and pricing. The property itself has not changed. The income used to qualify it has.

For a broader breakdown of how DSCR loans are structured in Idaho, you can start here:

https://www.dscrfinancing.com/dscr-loans-idaho/

Why Lender Selection Changes the Outcome

Not all lenders treat rent the same way, and many investors do not realize the difference until the refinance is already in process.

Some lenders will only use lease income. In these cases, even if the property is significantly under market, the lower number governs the qualification. Other lenders rely primarily on the appraised market rent, which is more common on vacant properties or in situations where the existing lease does not reflect current conditions. A third group allows the higher of the two, using either lease or market rent depending on which produces a stronger DSCR.

This is where many deals get misread. Investors often conclude the property does not qualify, when the actual issue is that the lender chosen did not align with the income profile of the property.

How This Shows Up on a Real Refinance

An investor in Nampa ran into this on a stabilized property. The existing lease was at $1,600, while the appraisal came back with a market rent of $1,900. The first lender underwrote the deal using lease income, which brought the DSCR in below their threshold and stopped the refinance. The second lender evaluated the same property using the higher of the two figures. With no other changes to the deal, the loan cleared and the refinance moved forward.

Nothing about the property changed. Nothing about the borrower changed. The only difference was which rent number the lender chose to use.

That difference is what determines whether capital comes back out of the property or stays trapped in the deal longer than expected.

Where This Shows Up Most in Idaho DSCR Deals

This issue appears consistently across specific property types and situations.

Properties with below-market tenants, where rents have not been adjusted over time, often depend on market rent to support the refinance. Recently renovated properties may not yet have stabilized lease income that reflects their updated condition. Vacant properties coming out of rehab rely on market rent to qualify at all. PadSplit and co-living models introduce an additional layer, where income may be higher in practice but not always recognized in a standard appraisal format.

Across the Treasure Valley, this dynamic plays out differently by location. Nampa and Caldwell tend to offer more flexibility due to lower entry prices and stronger rent-to-value relationships. Meridian sits in a more balanced position. Boise is tighter, where smaller differences in rent assumptions can affect loan outcomes more quickly.

How This Affects BRRRR Strategy in Idaho

This issue becomes most visible in BRRRR transactions, where the refinance is the step that determines whether capital comes back out or stays in the deal.

An investor buys a property below market, completes the rehab, and prepares to refinance. At that point, rents may still be catching up to market levels. If the lender qualifies using lease rent, the DSCR may fall short, limiting refinance proceeds or delaying the transaction. If market rent is used, the same property may meet DSCR requirements and allow capital to be recycled back into the next deal.

That is not a minor detail. It determines whether the BRRRR cycle continues or pauses.

For a closer look at how BRRRR deals are structured in Idaho using DSCR financing, you can read more here:

https://www.dscrfinancing.com/dscr-brrrr-strategy-idaho/

How Investors Structure Around This

Investors who execute consistently on these deals are not discovering the rent calculation issue during the refinance. They are accounting for it before they close.

Before structuring the deal, they confirm which rent figure the lender will use, what the property is likely to appraise for after improvements, and whether the projected DSCR holds under the lender’s specific income methodology. That alignment between lender guidelines and deal structure is what keeps timelines intact and capital moving on schedule.

Common Missteps

The most common issue is assuming all lenders treat rent the same way. An investor underwrites a deal using projected market rent, only to find out at the refinance stage that the lender is using the lease. The DSCR drops and the loan no longer lines up with the original plan.

A second misstep shows up on the appraisal side. The appraiser pulls rental comps from a different part of the market where rents run lower. Market rent comes in lighter than expected, the DSCR tightens, and the loan structure changes. This happens more often than investors expect, particularly in markets where rental comps vary significantly by neighborhood.

A third issue involves timing. Some deals are underwritten around rent increases that have not yet happened. The property supports the plan long term, but the refinance is based on where income stands today. That gap between current performance and projected performance is where many refinances get delayed.

Frequently Asked Questions About Market Rent vs Lease Rent in DSCR Loans

Do all DSCR lenders use market rent?

No. Some lenders use lease income only, some use market rent from the appraisal, and some allow the higher of the two. Which approach a lender uses can determine whether a deal qualifies, so confirming this before structuring the loan is worth doing early.

Can you qualify a vacant property for a DSCR loan?

Yes, if the lender allows market rent from the appraisal. Not every lender will proceed on a vacant property, but those that do use the 1007 rent schedule to establish projected income. This is particularly relevant for investors refinancing out of a rehab before placing a tenant.

Why does the rent figure matter so much in DSCR lending?

Because DSCR is calculated entirely on income relative to the monthly payment. A shift of $200 to $300 in recognized rent can move a deal from below a 1.0 ratio to above it, or change the available LTV and pricing. The income figure is the most sensitive variable in the qualification.

Is this more important in certain Idaho markets?

Yes. In tighter markets like Boise, where the spread between purchase price and rent is narrower, smaller differences in rent assumptions affect loan outcomes more quickly. In Nampa and Caldwell, the rent-to-value relationship tends to offer more room, but the same calculation applies.

What is the 1007 rent schedule?

The 1007 is a form completed by the appraiser that documents estimated market rent for the subject property. It is the standard source for market rent in DSCR underwriting and is used by lenders who qualify based on appraised income rather than the existing lease.

Working With the Right Lender on This

The rent calculation methodology is one of the most consequential lender-specific variables in DSCR lending, and it is rarely discussed until a deal is already in process. Knowing which lenders use lease rent, which use market rent, and which allow the higher of the two is part of matching the deal to the right program before the purchase closes.

For a full breakdown of how DSCR lenders in Idaho differ from each other and what to look for when evaluating them, you can read more here:

https://www.dscrfinancing.com/dscr-lenders-idaho/

About The Author

Patrick Penner is an Idaho DSCR mortgage strategist specializing in investor financing, co-living properties, Airbnb financing, rural investment properties, and portfolio growth strategies. Through Coast2Coast Mortgage, he works with investors nationwide to structure financing around long-term scalability, leverage, and property performance.

Learn more about Patrick Penner:

https://www.dscrfinancing.com/about/

Learn more about DSCR loans in Idaho:

https://www.dscrfinancing.com/dscr-loans-idaho/